Your credit score matters. A low score locks you out of better interest rates, higher credit limits, and financial opportunities that could save you thousands of dollars.

At Financial Canadian, we’ve seen firsthand how the best secured cards in Canada can turn your credit around. These cards give you a practical path forward when traditional lenders won’t take a chance on you.

How Secured Cards Actually Work

A secured card operates on a straightforward principle: you deposit cash into a linked account, and that deposit becomes your credit limit. The Neo Secured Mastercard requires a minimum deposit of just $50, making it accessible for people starting from scratch. Home Trust Secured Visa Card allows deposits ranging from $500 up to $10,000, giving you control over how much credit you want to establish. Your deposit sits there untouched-it’s collateral, not payment. You spend against your credit limit just like any other card, and you pay monthly bills from your regular income. This structure removes the lender’s risk, which is why approval happens instantly with cards like Neo. The deposit gets refunded when you close the account with no outstanding balance, so you’re not losing money long-term; you’re investing it in your credit future.

Building Real Credit While You Spend

The critical difference between a secured card and a prepaid card is that secured cards report to Equifax and TransUnion. Every payment you make gets recorded on your credit file. This is where the actual credit-building happens. If you spend $100 on groceries and pay it off on time, that positive payment history sticks to your credit report. Capital One Guaranteed Secured Mastercard charges no annual fee and reports to both major bureaus, making it a practical choice if you want to keep costs down. Treat the card like a debit card-spend small amounts you can actually pay off. Keep your monthly spending under 30% of your limit. If your limit is $500, spend no more than $150 monthly.

This low utilization ratio signals responsible credit management to lenders. Pay the full balance every month, not just the minimum. Interest rates on secured cards run between 19.99% and 29.99%, so carrying a balance defeats the entire purpose. Track your progress using TransUnion’s CreditView or Equifax Core Credit to see your score climb as you build payment history.

When You’re Ready to Graduate

Most people move to an unsecured card within 6 to 12 months of responsible use. Some issuers, including Neo, offer a clear upgrade path-you can graduate to the Neo World Mastercard once your credit improves. When you upgrade, your deposit returns to your account, and you get access to better rewards and benefits. A credit score around 660 or higher typically qualifies you for unsecured options. The transition isn’t automatic; you need to apply for the new card. At that point, you’ll have proof of on-time payments and responsible credit use to back your application. Late payments wreck this timeline completely-even one missed payment can set you back months because it stays on your report for years. Once you understand how secured cards work and what it takes to graduate, the next step is identifying which card matches your financial situation and goals.

Which Secured Card Gives You the Best Value

Comparing Your Top Options

Neo Secured Mastercard stands out as the lowest-cost entry point with its $50 minimum deposit, but that accessibility comes with a trade-off. Neo charges $7.99 monthly, which totals $95.88 per year-higher than cards with no annual fee. However, instant approval and 1% cash back on gas and groceries make it worthwhile if you plan to use the card regularly. Capital One Guaranteed Secured Mastercard eliminates the annual fee entirely at $0, requires only a $75 minimum deposit, and reports to both Equifax and TransUnion.

The catch: Capital One’s APR ranges from 21.9% to 29.9%, slightly higher than Neo’s range. Home Trust Secured Visa Card offers zero annual fees and accepts deposits from $500 to $10,000, but it’s unavailable in Quebec, which immediately disqualifies it for a significant portion of Canadian consumers. If you live outside Quebec and can deposit $500 upfront, Home Trust becomes the cheapest long-term option.

The Neo World Mastercard serves as your upgrade path once your credit improves, requiring a $200 deposit and charging $149 annually. It includes travel insurance, rental car coverage, and trip cancellation protection up to $5,000-genuine value if you travel. Your choice depends on whether you prioritize instant approval and rewards (Neo Secured) or lowest fees and accessibility (Capital One). Avoid the trap of paying monthly fees on a card you barely use; the deposit alone ties up your cash, so you need to justify every dollar in charges.

Understanding Approval Odds and Credit Checks

Your approval odds matter more than the fee structure if you have poor or no credit history. Neo Secured Mastercard offers no hard inquiry to apply, meaning you won’t see a dip in your credit score just from applying. Capital One and Home Trust perform soft checks initially, then a hard check only if you’re approved, reducing unnecessary damage to your file. Ratehub’s CardFinder tool lets you run a soft check first to gauge your actual approval odds before submitting a full application, preventing multiple hard inquiries that compound your credit damage.

Newcomers to Canada face additional barriers because traditional lenders view them as high-risk, but secured cards bypass this problem entirely since your deposit covers the lender’s risk. Your credit score at application doesn’t matter for secured cards the way it does for unsecured products-the collateral removes that variable. What matters is your income verification and identity confirmation.

Tracking Your Path to Graduation

After 6 to 12 months of on-time payments, your credit score will climb enough to qualify for unsecured options. Track this progress using TransUnion’s ScoreSimulator, which shows you exactly how different spending and payment patterns affect your score before they actually happen. This tool eliminates guesswork and lets you plan your upgrade timeline with confidence. Once you understand which card fits your situation and how approval works, the next step involves using that card strategically to build the strongest possible credit foundation.

How to Build Credit Faster With a Secured Card

Set Up Autopay to Lock In Perfect Payments

On-time payments are non-negotiable if you want your credit score to climb. A single missed payment tanks your progress because that late payment stays on your credit report for up to seven years and damages your score far more than one on-time payment helps it. Set up automatic payments from your chequing account on the day you get paid, before you spend that money on anything else. This removes the possibility of forgetting and keeps your payment history spotless. Capital One Guaranteed Secured Mastercard and Neo Secured Mastercard both support autopay, so there’s no excuse for manual slip-ups.

After three months of perfect payments, your credit score typically rises 10 to 20 points. After six months, you’re looking at 30 to 50 points of improvement, assuming you manage your credit utilization properly. TransUnion’s CreditView lets you monitor this progress weekly, so you’ll see the exact impact of your discipline. The moment you miss a payment, that progress stops and reverses. One late payment can erase six months of work, which is why autopay isn’t optional-it’s your foundation.

Keep Your Utilization Ratio Aggressively Low

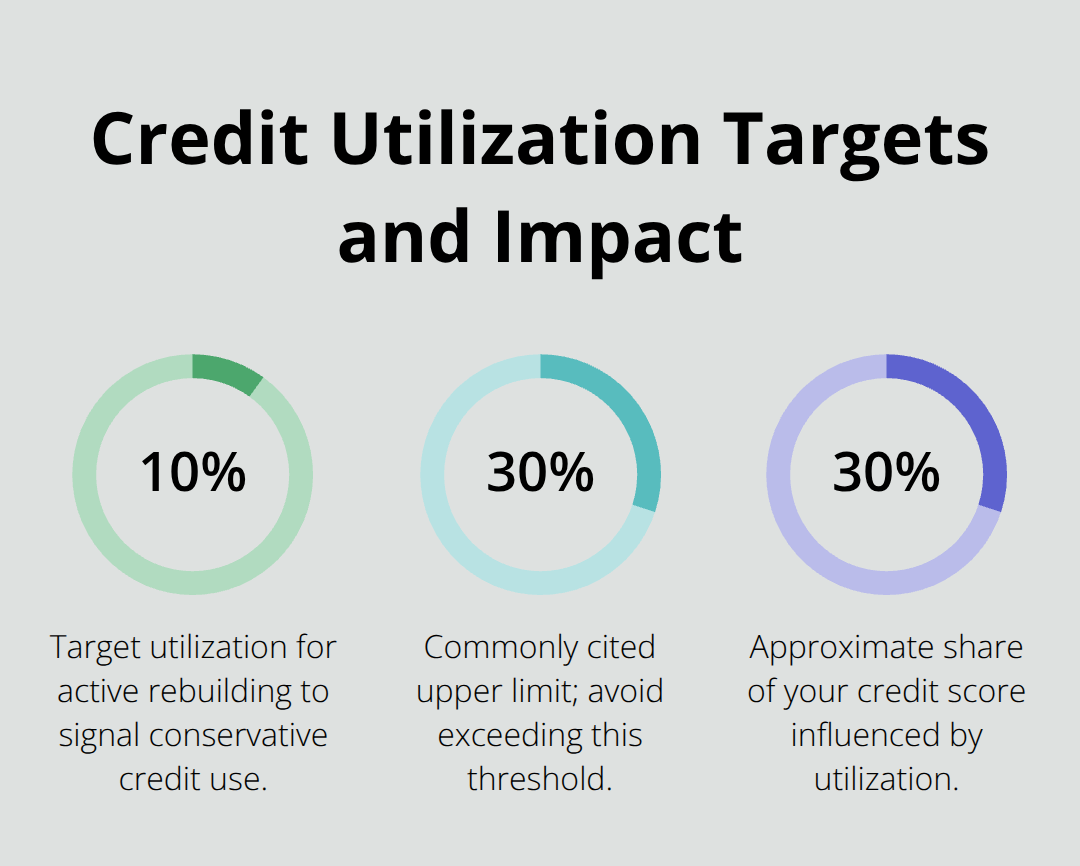

Credit utilization ratio matters just as much as payment history, and most people misunderstand how aggressively to manage it. The conventional wisdom says stay under 30%, but we think that’s too high if you’re actively rebuilding. Try for under 10% of your credit limit. If your limit is $500, spend no more than $50 monthly and pay it off immediately. This signals to Equifax and TransUnion that you’re not desperate for credit and that you manage money conservatively.

High utilization-anything above 30%-makes lenders think you’re financially stretched, which kills your score even if you pay on time. Your utilization ratio accounts for roughly 30% of your credit score, making it your second-most important lever after payment history. The good news is that utilization changes immediately when you pay down your balance, unlike payment history which takes months to show impact. Pay your balance mid-cycle if you can, not just at the statement due date. This means if your card cycles on the 15th, pay your balance on the 10th so the reporting agencies see a low utilization snapshot.

Catch and Dispute Credit Report Errors

Monitoring your credit report quarterly through Equifax Core Credit or TransUnion’s free annual report catches errors before they damage your score further. Dispute any inaccuracies immediately-a single reporting error can cost you 50 to 100 points unnecessarily. Errors happen more often than most people realize (especially for newcomers or those with limited credit history), so don’t assume your report is accurate just because you haven’t checked it. Pull your report, read it carefully, and flag anything that doesn’t match your actual payment history or account status.

These three actions-autopay, aggressive utilization management, and error monitoring-compound together to accelerate your timeline to an unsecured card from 12 months down to 6 to 8 months.

Final Thoughts

Secured cards work because they remove the guesswork from credit building. You deposit cash, spend responsibly, pay on time, and watch your score climb. The best secured cards in Canada give you multiple pathways forward depending on your situation-if you need instant approval and don’t mind a monthly fee, Neo Secured Mastercard gets you started with just $50, while Capital One or Home Trust become your better long-term choices if you want zero annual costs.

Your timeline to graduation depends entirely on execution. Six to eight months of perfect payments, aggressive utilization management under 10%, and quarterly credit report monitoring can get you to an unsecured card faster than most people expect. One missed payment resets everything, so autopay isn’t optional, and one month of high spending above 30% utilization damages your score immediately, so track every purchase.

Your next step is choosing which card matches your deposit capacity and approval timeline, then setting up autopay before you make your first purchase. We at Financial Canadian help you establish strong financial foundations through practical guides and actionable strategies that drive real results. Apply the same principle to your credit: build it right from the start, and everything else becomes easier.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment