When you need cash fast, online payday loans in Canada can seem like the quickest solution. But the reality is far more complicated than a simple application and quick payout.

At Financial Canadian, we’ve seen too many borrowers trapped by sky-high interest rates and hidden fees that turn a short-term fix into a long-term financial nightmare. This guide walks you through exactly what you’re signing up for-and better options that won’t drain your bank account.

How Online Payday Loans Actually Work

The Application and Approval Process

Online payday lenders in Canada approve applications within hours, not days. You complete an online form with your income, employment status, and bank details, and most lenders provide instant approval without checking your credit history. Once approved, funds arrive via e-transfer directly to your account, often within the same day or by the next morning. Lenders remove friction from the process because they profit from volume, not careful underwriting. This speed masks a steep price tag that catches most borrowers off guard.

Understanding the True Cost of Borrowing

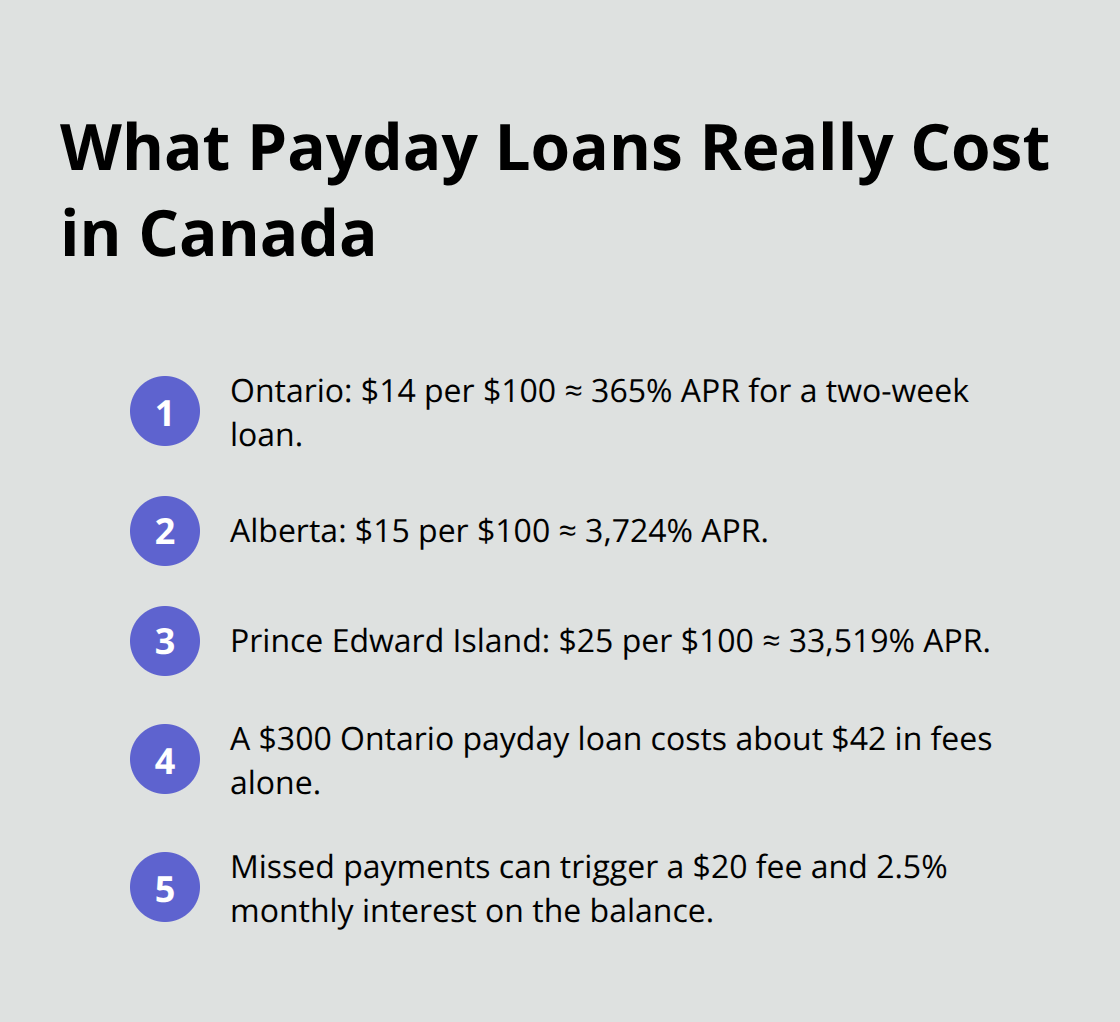

Ontario allows lenders to charge a maximum of $14 per $100 borrowed as of January 2025, which equals an effective annual percentage rate of roughly 365% for a two-week loan. Alberta caps charges at $15 per $100, but that still translates to approximately 3,724% APR. A typical $300 loan in Ontario costs about $42 in fees alone. Prince Edward Island permits $25 per $100, creating an astronomically high effective annual rate of roughly 33,519%. These numbers illustrate why payday loans represent the most expensive consumer credit available in Canada. Repayment occurs on your next payday, usually two to four weeks after you borrow.

Lenders require either a post-dated cheque or pre-authorized debit authorization from your bank account. If your cheque bounces or the debit fails, you face a $20 dishonoured payment fee under current Ontario rules. Missing a payment triggers a maximum monthly interest rate of 2.5% on the outstanding balance, compounding your debt further.

Provincial Regulations Create Vastly Different Costs

Each province sets its own rules, creating dramatically different costs for borrowers. Ontario, Alberta, and British Columbia have implemented stricter caps compared to provinces like Prince Edward Island or Newfoundland and Labrador, where rates remain extraordinarily high. British Columbia requires lenders to register with Consumer Protection BC and allows cancellation within one business day without penalty. New Brunswick mandates that loans cannot exceed 30% of your net pay, protecting borrowers from over-borrowing. Alberta and Saskatchewan require licenses, though enforcement varies. Newfoundland and Labrador lacks provincial payday-loan legislation entirely, meaning the federal limit applies in practice, but this remains largely unenforced.

Verifying Lender Legitimacy and Contract Terms

Before you borrow online, verify your lender’s license with your provincial regulator. Ontario lenders must display their license number prominently on contracts. Many online platforms operate across provincial borders, so confirm the lender complies with your province’s specific rules. Rollover loans-extending debt by taking a new loan with the same lender-are prohibited in Ontario and most provinces, yet some lenders still pressure borrowers into this cycle through aggressive renewal tactics. The first page of any loan contract must clearly show the amount borrowed, the exact loan term, and the total cost of borrowing. If a lender cannot provide this transparent disclosure upfront, walk away immediately. Understanding these mechanics sets the stage for recognizing the real dangers that trap borrowers in cycles of debt.

Why Payday Loans Trap You in Debt

The Rollover Cycle That Destroys Your Finances

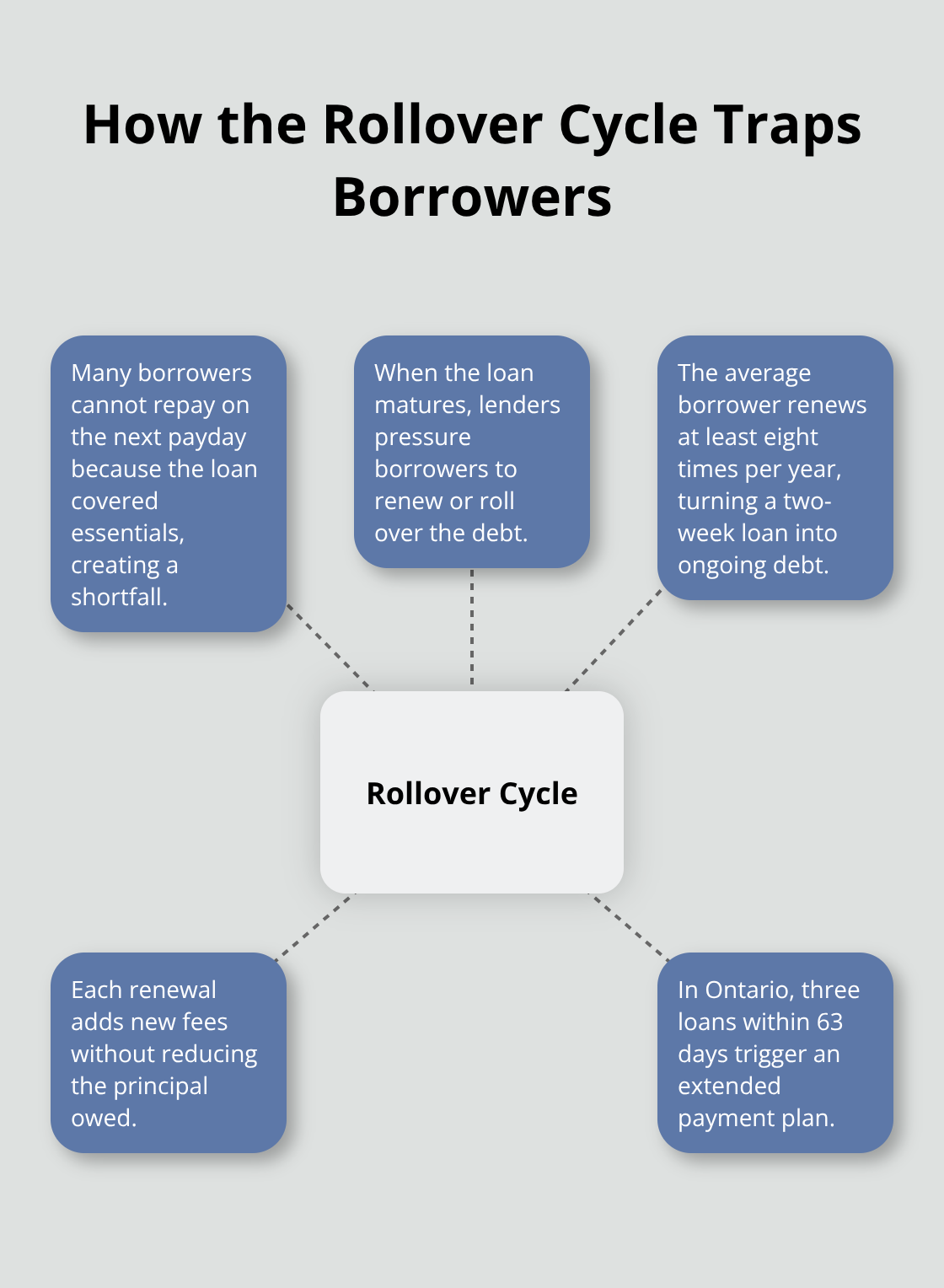

The real danger of payday loans isn’t the initial interest rate-it’s what happens when that first loan comes due. Most borrowers cannot repay the full amount on their next payday because the loan consumed money they desperately needed for rent, food, or utilities. When the loan matures, lenders pressure borrowers to renew or roll over the debt into a fresh loan. This rollover cycle is where payday lending becomes predatory.

A borrower who takes three payday loans within 63 days in Ontario enters an extended payment plan, yet many borrowers hit this threshold without realizing they’ve crossed into a debt spiral. Research shows that the average payday borrower renews their loan at least eight times per year, transforming a two-week emergency into a permanent financial burden. Each renewal adds another round of fees, and this fee does not reduce the amount you owe.

The True Cost of Repeated Borrowing

Lenders design their business model around this predictable cycle. They make more money from borrowers who roll over repeatedly than from those who repay on time. Aggressive renewal tactics-emails, phone calls, and automatic payment authorizations-keep borrowers trapped.

If you miss a payment or cannot renew, lenders file collections claims and can pursue wage garnishment, which means money is deducted directly from your paycheck before you see it. This devastates your ability to cover basic living expenses and forces you into an even tighter financial corner.

How Payday Debt Damages Your Credit and Future

The damage extends beyond immediate fees. Missed payday loan payments get reported to collections agencies, and collections accounts remain on your credit report for up to 6 years. This destroys your credit score, making it nearly impossible to qualify for a mortgage, car loan, or credit card at reasonable rates.

When you eventually need credit for something legitimate-a home purchase or emergency car repair-lenders view you as high-risk and charge you 5% to 10% more in interest. Over a 25-year mortgage, that premium costs you tens of thousands of dollars. The payday loan trap extends far beyond the initial two-week term.

Addressing the Root Problem, Not Just the Symptom

Payday loans also mask deeper financial problems rather than solving them. Taking a payday loan when you cannot cover basic expenses signals that your income is too low or your expenses are too high. Without addressing the root cause, you will return to payday lending repeatedly. This is why government assistance programs and credit counseling exist-to help you fix the underlying problem, not just patch it temporarily.

Contact Money Mentors in Red Deer, Alberta or local nonprofits in your province for free budgeting advice before borrowing. They help you build a realistic plan to cover shortfalls without accumulating debt. Understanding what drives you to payday lending in the first place is the only way to break free from the cycle and move toward genuine financial stability. The alternatives available to you-from personal loans to government programs-offer real solutions that address both your immediate cash need and your long-term financial health.

Better Borrowing Options That Actually Work

Personal Loans and Credit Union Alternatives

A bank personal loan or credit union small-dollar loan costs dramatically less than payday debt. Banks typically charge between 7% and 21% annual interest on personal loans, depending on your credit score, compared to the 365% to 14,000%+ APR you face with payday lenders. Credit unions often undercut banks further, offering lower rates and fees because they prioritize member welfare over shareholder returns. The catch is that banks require a credit check and proof of income, which means you need at least decent credit to qualify. If your credit score sits below 600, most banks will reject you outright. However, if you have any credit history at all, a personal loan from a credit union beats payday lending every single time.

Lines of Credit and Overdraft Protection

Unsecured lines of credit from banks work similarly, giving you access to funds up to a set limit at interest rates between 7% and 15% annually. You only pay interest on what you actually borrow, not the full available credit. Overdraft protection, while expensive at typical rates of 21%, still costs far less than a payday loan if you only use it for a few days. The real advantage of these options is that they do not trap you in a rollover cycle. You make fixed monthly payments that actually reduce what you owe, unlike payday loans where fees pile up without touching principal.

Government Assistance and Nonprofit Resources

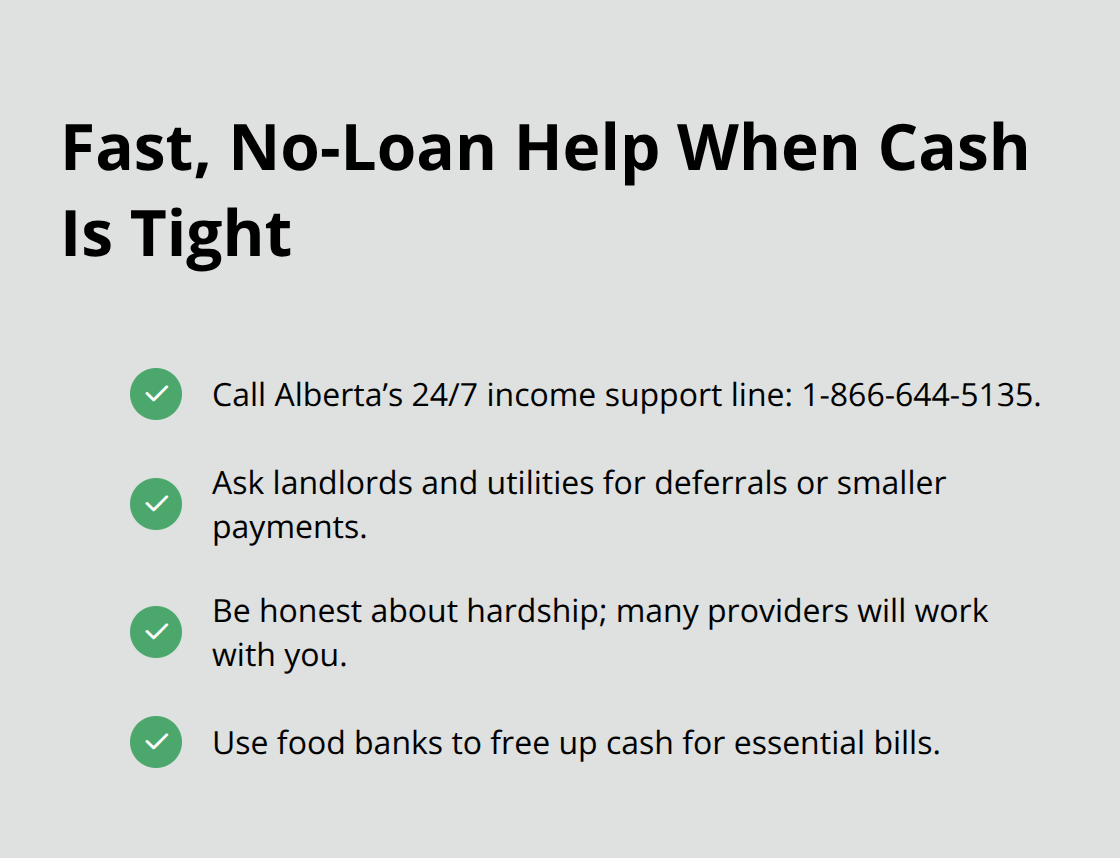

Government assistance programs and nonprofit credit counseling offer the fastest path out of financial crisis without borrowing at all. Alberta provides income support through its 24/7 helpline at 1-866-644-5135, and the province’s website lists emergency assistance options you can access immediately. Contact your landlord, utilities, and other creditors to negotiate payment deferrals or arrange smaller goodwill payments that buy you time. Most service providers will work with you if you communicate honestly about hardship rather than disappearing.

Food banks provide immediate relief on groceries, freeing up cash for essential bills.

Practical Steps to Avoid Borrowing

Money Mentors in Red Deer and similar nonprofits across Canada offer free budgeting counseling to help you identify where money actually goes and where you can cut without destroying your quality of life. Many borrowers discover they can cover shortfalls through overtime work, selling unused items online, or postponing discretionary spending rather than borrowing. The Alberta Food Bank, Edmonton Food Bank, and community organizations in your area offer practical assistance that costs you nothing. These resources exist specifically because payday loans solve nothing-they only delay the real problem while charging you thousands in fees.

Final Thoughts

Online payday loans in Canada trap borrowers in expensive cycles that destroy financial stability. A $300 loan that costs $42 in fees seems manageable until you cannot repay it on your next payday, then the lender pressures you to renew, adding another $42 in fees while the original $300 remains unpaid. After eight renewals-the average for payday borrowers-you have paid $336 in fees alone without reducing what you owe, and collections accounts follow as your credit score plummets.

Personal loans from banks or credit unions cost between 7% and 21% annually, a fraction of payday lending’s 365% to 14,000%+ rates, and they eliminate the rollover cycle entirely. Lines of credit and overdraft protection offer similar advantages without the predatory pressure to renew repeatedly. If borrowing feels impossible, government assistance programs and nonprofit credit counseling provide real solutions that address the root cause of your cash shortage rather than masking it with expensive debt.

Before you apply for any loan, ask yourself three questions: Does this lender appear in your provincial regulator’s database? Does the contract clearly show the total cost of borrowing? Can you realistically repay this on your next payday without sacrificing food or housing? If you answer no to any question, walk away and contact Money Mentors or a local nonprofit instead-we at Financial Canadian help you build a strong financial strategy that protects your long-term stability over short-term convenience.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment