Your credit score directly affects your ability to borrow money, rent an apartment, or even land certain jobs in Canada. A low rating can cost you thousands in higher interest rates.

At Financial Canadian, we’ve created this guide to show you exactly how to improve your Canada credit score through concrete, actionable steps. You’ll learn what actually moves the needle and how quickly you can see real results.

How Your Credit Score Works in Canada

Your credit score is a three-digit number between 300 and 900 that lenders use to decide whether to approve you for credit and what interest rate to charge. In Canada, two credit bureaus dominate: Equifax and TransUnion. Both collect your financial behavior and calculate scores independently, which means your score can differ between them. This matters because lenders may check only one bureau, so a weak score at Equifax could still hurt you even if TransUnion shows something better. You cannot control which bureau a lender uses, which is why monitoring both matters. The gap between your scores at each bureau typically ranges from 10 to 50 points, depending on how recently each one updated your information. Most lenders report to both bureaus monthly, but timing varies, so your scores shift at different times each month.

What Actually Moves Your Score

Payment history dominates your score, accounting for roughly 35% of the calculation. A single late payment can drop your score by 50 to 100 points immediately, while consistent on-time payments rebuild it gradually over months. Credit utilization-the percentage of your available credit you actually use-accounts for about 30% of your score.

If you have a $5,000 credit limit and carry a $3,500 balance, your utilization is 70%, which signals risk to lenders. Dropping that same balance to $1,500 brings your utilization to 30% and triggers a meaningful score increase, often within 30 to 45 days once the bureau updates. The length of your credit history makes up roughly 15% of your score, which is why closing old accounts after paying them off actively hurts you. Keep that first credit card open for years, even if unused, to protect your score more than closing it ever will. Hard inquiries and credit mix each account for 10% of your score. Hard inquiries occur when you apply for new credit, and multiple applications in a short period signal financial desperation to lenders, dropping your score by 5 to 10 points each. Credit mix means having both revolving credit like credit cards and installment loans like car payments or mortgages strengthens your score.

What Does Not Affect Your Score

Checking your own credit report does not affect your score at all-this is a soft inquiry that lenders cannot see. You can pull your report free once yearly from both Equifax and TransUnion without penalty. Your income level never appears on your credit report and has zero impact on your score, though lenders may consider it separately during approval decisions. A debit card used exclusively will not build your credit at all because debit transactions do not get reported to credit bureaus. High-interest-rate loans themselves do not damage your score unless you miss payments on them. This means a payday loan at 400% interest will not lower your score if you pay it on time, though the interest cost will drain your finances regardless.

Why Most Canadians Waste Time on Wrong Tactics

Many Canadians waste months pursuing tactics that do not move the needle, like obsessively monitoring their score or avoiding debit cards. The real work happens through consistent on-time payments and keeping your utilization low. These two factors alone account for 65% of your score, yet most people focus on minor adjustments that produce no measurable results. Understanding what actually matters sets you up to make progress fast. With this foundation in place, you can now move to the specific actions that will raise your rating.

How to Raise Your Credit Score Fast

Attack Payment History and Credit Utilization First

The fastest way to raise your credit score targets the two factors that matter most: payment history and credit utilization. These two alone account for a significant portion of your score, with credit utilization ratio often being the second most important factor following payment history. Start with payment history immediately by setting up automatic payments on every credit card and loan for at least the minimum amount due, scheduled two days before the due date to account for processing delays. Late payments destroy your score far more than anything else, and autopay eliminates human error entirely.

If you have missed payments in the past, contact your lender directly and ask about a goodwill adjustment. Some lenders will remove a single late payment from your report if you have otherwise paid on time for the past year. This costs nothing and can recover 50 to 100 points instantly.

Lower Your Credit Utilization Ratio

For credit utilization, the math is straightforward: if your credit cards are maxed out, your score will not improve much no matter what else you do. Request a credit limit increase on your existing cards without a hard inquiry, which some issuers allow through their online portals or by phone. This lowers your utilization ratio immediately without a new application triggering a hard inquiry.

If your cards remain high-balance, pay them down aggressively each month until you hit the 30% utilization threshold. A $5,000 card should carry no more than a $1,500 balance. Expect to see score improvements within 30 to 45 days after the bureaus update your information.

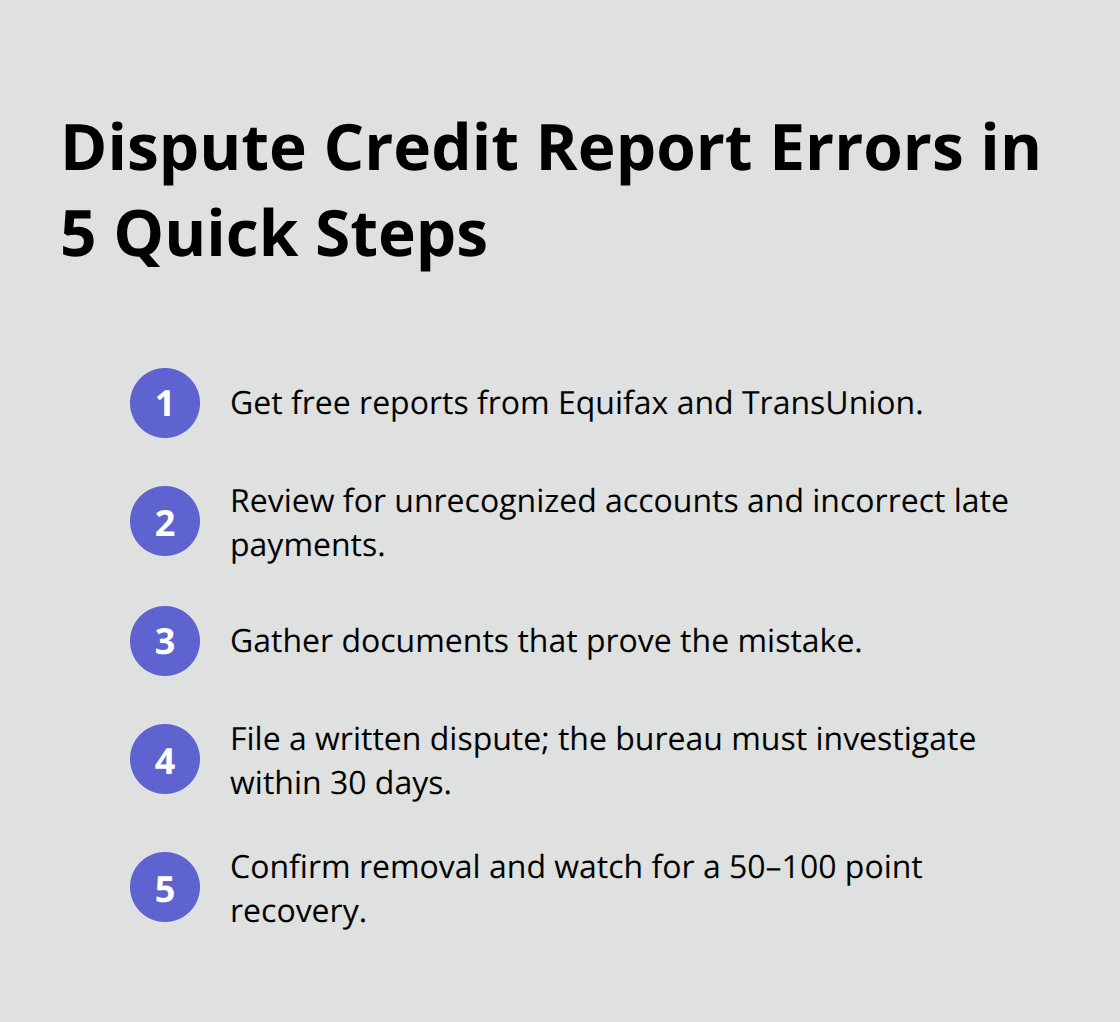

Identify and Dispute Reporting Errors

Pull your credit reports from both Equifax and TransUnion at no cost through their websites once per year. Look specifically for accounts you do not recognize, late payments you never made, or duplicate entries. Errors happen frequently and can drop your score unnecessarily.

If you find an inaccuracy, file a dispute directly with the bureau in writing, including documentation that proves the error. The bureau must investigate within 30 days and remove incorrect information. This single step has recovered 50 to 100 points for people with significant reporting errors.

Skip Authorized User Shortcuts

Do not waste time on becoming an authorized user as a shortcut to building credit. While adding yourself to someone else’s old account with perfect payment history sounds appealing, most banks now exclude authorized users from credit scoring calculations. Instead, focus your energy on your own accounts and your own payment history, which always counts.

If your credit history is very thin and you have no established accounts, a credit-builder loan serves this purpose far better than chasing authorized user status. These loans let you build a payment history while the lender holds your deposit as collateral. Once you complete the loan term, you recover your deposit plus interest, and your payment history strengthens your score significantly.

With these tactical fixes in place, you now need tools to track your progress and monitor both bureaus consistently.

How to Track Your Credit Progress

Monitoring your credit across both bureaus matters far more than most people realize, yet most Canadians check their scores sporadically and miss critical changes. You need a system that tracks both Equifax and TransUnion simultaneously, alerts you to errors before they damage your rating, and shows you exactly when your improvements register.

Access Free Credit Reports and Monitoring

Equifax and TransUnion both allow free annual credit report access through their official websites, but this once-yearly window leaves you blind for eleven months. A better approach uses free credit monitoring services that update more frequently. Core Credit provides daily access to your Equifax credit report and VantageScore at no cost, letting you watch your utilization ratio drop and your score climb in real time as you pay down balances. This daily visibility matters because you can confirm whether your payment hit the bureau’s system and when your score responds, typically within 30 to 45 days. TransUnion offers similar free monitoring through their online portal, giving you visibility into the second major bureau. Checking both services takes five minutes monthly and costs nothing.

Avoid Unnecessary Premium Services

Many Canadians purchase premium credit monitoring with identity theft protection, but this adds unnecessary expense when free options already track the metrics that matter most. The free tier from both bureaus covers score tracking and error detection without the premium price tag.

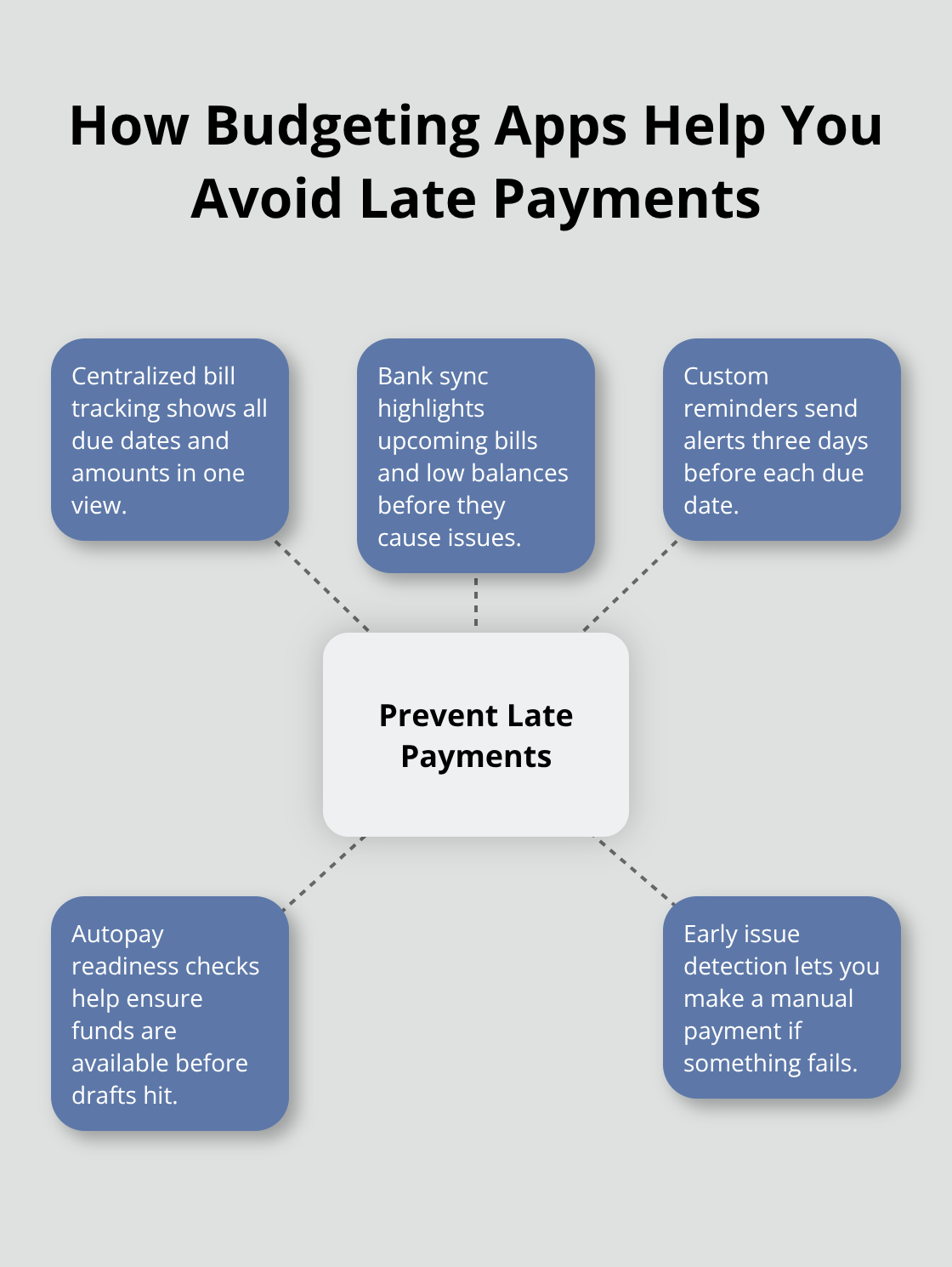

Use Budgeting Apps to Prevent Late Payments

For payment tracking specifically, a budgeting app prevents late payments far better than calendar reminders or bank notifications alone. Apps like YNAB and Wealthsimple track your spending categories and upcoming bills in one dashboard, showing you exactly when payments hit and how much buffer you have before due dates. These apps integrate with your bank accounts and highlight bills scheduled within the next week, eliminating the excuse of a forgotten payment. Set your app to send notifications three days before each due date, giving you time to verify funds are available before autopay triggers.

This approach catches problems early, like insufficient funds or a failed transaction, when you can still manually pay rather than discovering a late payment after it damages your score.

Combine Monitoring Tools for Maximum Accountability

The combination of daily credit monitoring plus a budgeting app creates accountability that most Canadians never achieve. You see your score improve monthly, track exactly which actions moved the needle, and maintain the payment discipline that keeps improvements permanent. This system transforms credit management from a quarterly afterthought into an active, visible process that produces measurable results.

Final Thoughts

Your Canada credit score improvement starts with two non-negotiable actions: paying bills on time and keeping your credit utilization below 30%. These two factors account for 65% of your score, so neglecting them wastes months on tactics that produce minimal results. Payment history improvements and credit utilization drops both appear within 30 to 45 days after the bureaus update your information, while disputing errors can recover 50 to 100 points instantly if inaccuracies exist on your report.

Maintaining your improved rating requires you to treat credit management as an ongoing habit rather than a one-time project. Set up autopay for every account and never disable it, monitor both Equifax and TransUnion monthly using their free tools, keep old accounts open even after you pay them off, and avoid applying for new credit unless absolutely necessary. Late payments take longer to fade; a single missed payment damages your score for six years, though its impact weakens after 12 to 24 months of perfect payments afterward.

We at Financial Canadian help you build strong financial foundations through expert guidance and resources that establish credibility and drive real progress. A solid foundation built through consistent habits produces lasting results far better than quick fixes ever will, and your improved score opens doors to better interest rates, easier loan approvals, and lower borrowing costs for years to come.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment