Borrowing money in Canada doesn’t have to be confusing. Whether you need a personal loan, auto financing, or debt consolidation, understanding your options matters.

At Financial Canadian, we’ve created this Canadian loan comparison guide to help you cut through the noise. We’ll show you how to compare rates, evaluate lenders, and find the loan that actually fits your situation.

Types of Loans Available to Canadian Borrowers

Personal Loans: Flexibility and Cost Variations

Personal loans remain the most flexible borrowing option in Canada, with APRs ranging from 6% to 35% depending on your credit profile and lender. Major banks like Scotiabank, CIBC, and RBC offer starting rates around 6%–10% for well-qualified borrowers, while online lenders such as Spring Financial, goPeer, and Mogo typically charge 9.99%–46.96%. The difference matters significantly: a $10,000 loan at 7% costs roughly $2,360 in interest over five years, whereas the same loan at 25% costs $6,790.

Personal loans work well for home renovations, medical bills, education costs, and consolidating high-interest credit card debt. You’ll find loan amounts from $500 to $200,000 across lenders, though eligibility depends on income (some accept $2,000 monthly, others require $17,000 annually), employment stability, and your debt-to-income ratio. Fixed-rate personal loans lock in predictable monthly payments, while variable-rate options tie to the Bank of Canada rate and can fluctuate monthly-an important distinction when you budget.

Auto Loans: Speed and Collateral Advantages

Auto loans deserve separate consideration because they typically process faster than unsecured personal loans and often deliver competitive rates since the vehicle itself serves as collateral. Banks and credit unions frequently offer auto financing with terms up to eight years, making monthly payments manageable for expensive purchases.

Debt Consolidation: Simplification With Trade-Offs

Debt consolidation loans specifically address the problem of juggling multiple creditors: they bundle existing debts into a single fixed payment, simplifying your finances immediately. However, consolidation loans often extend your repayment term, which means you’ll pay more total interest despite lower monthly payments-always compare the total interest cost before committing. The 35% APR cap protects Canadian borrowers from predatory lending, but rates still vary enormously based on your creditworthiness and the lender’s risk assessment.

Secured vs. Unsecured: Weighing Risk and Cost

When you evaluate which loan type fits your needs, focus on three concrete factors: the total cost in dollars (not just the interest rate), your ability to repay without stretching your budget, and whether prepayment penalties apply. A secured loan backed by your home or vehicle typically offers lower rates-often 2%–5% below unsecured options-but puts your asset at risk if you default. Unsecured personal loans avoid collateral requirements, delivering faster approvals and less paperwork, though you’ll pay higher interest for that convenience.

Preparing to Compare: Credit Scores and Hidden Fees

Check your credit score with Equifax Canada or TransUnion Canada before you shop, as this directly influences both approval odds and the rates lenders offer you. Origination fees ranging from 0.5% to 8% add hidden costs that aren’t reflected in advertised interest rates alone-always compare APR rather than the headline rate, since APR includes these fees and shows the true annual cost. The Bank of Canada held the overnight rate at 2.25% in early 2026, which helps stabilize personal loan pricing across lenders, meaning you’ll find more predictable rates than during volatile rate environments. Use online comparison tools to view personalized offers in about 60 seconds without damaging your credit score, then evaluate total cost, fees, and prepayment flexibility across multiple high-authority sources before you decide. With these loan types and their mechanics clear, you’re ready to learn how to compare them effectively online.

Comparing Loans Online Without Wasting Time

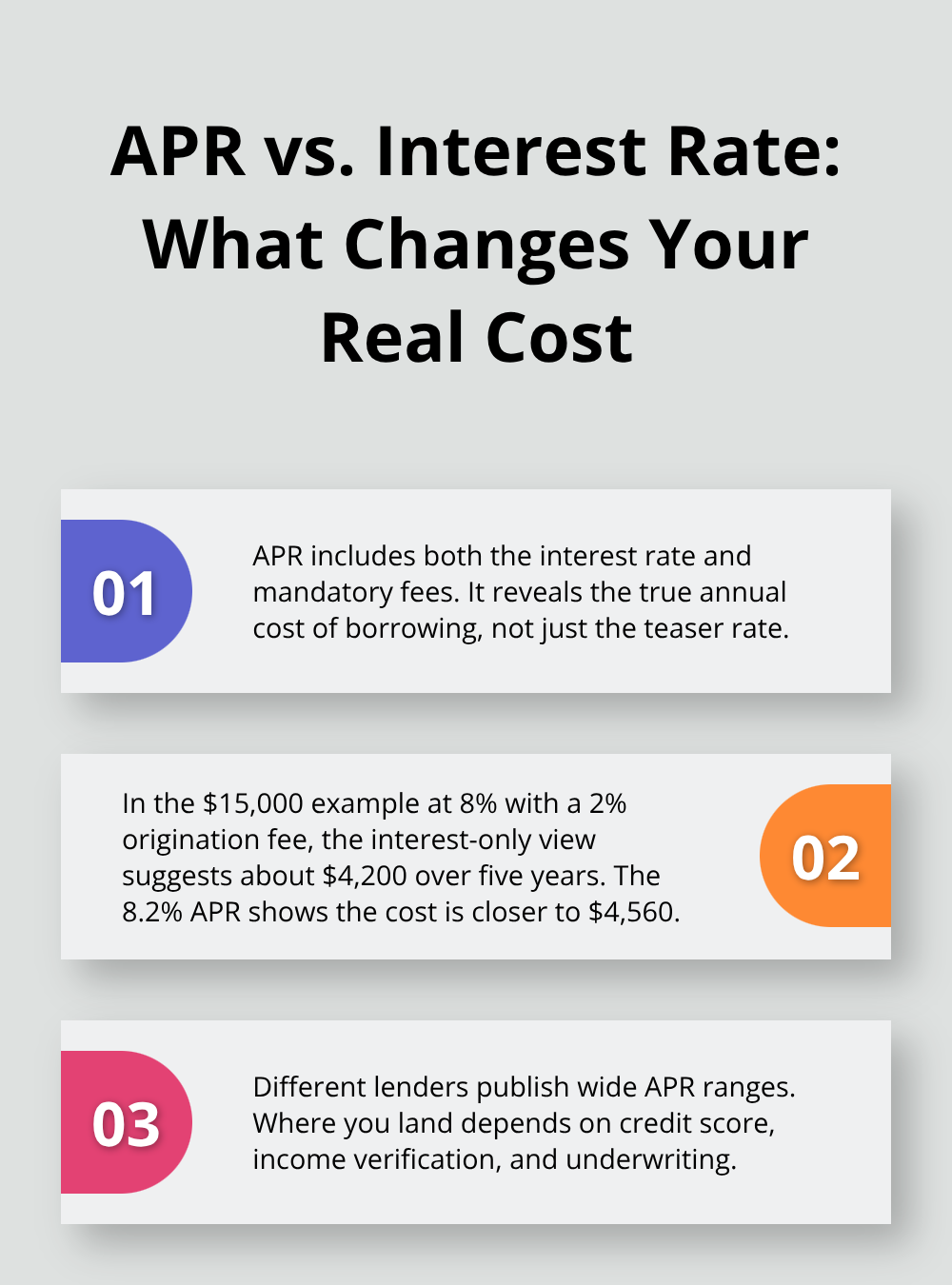

Understanding APR: The True Cost of Borrowing

APR reveals everything the advertised interest rate hides. When Scotiabank advertises a personal loan at 6%, that’s just the starting rate for borrowers with excellent credit-the APR includes origination fees, and shows the true annual cost. A $15,000 loan at 8% with a 2% origination fee ($300) costs roughly $4,200 in total interest over five years if you only look at the rate, but the APR of 8.2% reveals you’re actually paying closer to $4,560.

Online lenders like Spring Financial and goPeer publish APR ranges of 9.99%–34.95% and 8.99%–34.99% respectively, which means your actual rate depends entirely on your credit score and income verification.

The term length matters equally: a five-year loan spreads payments across 60 months while an eight-year auto loan stretches to 96 months, lowering your monthly payment but increasing total interest paid significantly. You should calculate the true monthly payment with CIBC’s online Loan and Line of Credit Calculator or similar tools from other major banks-these show you exactly what you’ll pay each month before you apply, preventing surprise sticker shock when approval arrives.

Using Comparison Tools Effectively

Comparison tools eliminate guesswork but only if you use them correctly. Ratehub.ca and similar platforms let you input your loan amount, desired term, and credit range in about 60 seconds and receive personalized APR offers without a hard credit inquiry damaging your score-this matters because multiple hard inquiries within two weeks can lower your credit score by 5–10 points. When you evaluate results, ignore lenders with poor customer reviews on independent sites like Trustpilot or Google Reviews; a lender offering 7% APR means nothing if they have a pattern of hidden fees or slow funding.

You should check whether the lender holds a license from the Financial Consumer Agency of Canada or operates under provincial regulation-unlicensed operators often hide behind aggressive marketing and predatory terms. Confirm prepayment policies before committing: some lenders charge 3–5% penalties if you pay off early, while others allow unlimited prepayment at no cost, which dramatically changes the loan’s true value if your financial situation improves.

Evaluating Rate Types and Lender Credentials

You need to ask specifically whether the lender offers variable or fixed rates and how rates adjust if you choose variable. You should request written quotes from at least three lenders showing the exact APR, term, monthly payment, and total cost before comparing, because phone quotes sometimes differ from final offers once underwriting reviews your full financial picture. These written quotes form the foundation for your final decision and protect you from unexpected changes during the approval process.

What Credit Score and Income Do You Actually Need

Credit Score Thresholds Across Canadian Lenders

Your credit score acts as the first gateway lenders evaluate, and the numbers matter more than you might think. Equifax Canada and TransUnion Canada track your score, which typically ranges from 300 to 900, and most Canadian banks won’t approve personal loans below 620 unless you accept significantly higher rates. Scotiabank requires 650+ for their best rates around 6%, while BMO and TD start approving at 580–600 but charge 8.99%–22.99% depending on your score tier. Online lenders like Spring Financial and goPeer accept scores as low as 580–600, but that flexibility comes at a cost: their APRs jump to 9.99%–34.95% and 8.99%–34.99% respectively for weaker credit profiles.

Check your score with Equifax or TransUnion before applying anywhere. If your score sits below 650, you have two realistic options. First, dispute any errors on your credit report (roughly 20% of Canadians have errors that lower their scores), which takes 30–45 days but sometimes improves your rating enough to qualify for better rates. Second, apply only with lenders who explicitly accept lower scores rather than submitting applications to banks that will automatically reject you, since each rejection triggers a hard inquiry that drops your score another 5–10 points.

Income Verification: What Lenders Actually Require

Income verification requirements vary dramatically across lenders and directly influence your approval odds. Some lenders accept $2,000 monthly income, while major banks like CIBC require minimum annual income around $17,000 before they’ll consider your application. Lenders care more about stable, verifiable income than the total amount. Self-employed applicants need two years of tax returns and business financial statements; salaried employees need recent pay stubs and an employment letter; and contract workers should provide signed contracts plus recent invoices.

The income documentation you submit forms the foundation of your application. Lenders verify employment through direct contact with your employer or by reviewing official records, so provide accurate information and notify your employer if they might receive verification calls. Gaps in employment history or frequent job changes can trigger additional scrutiny, though this doesn’t automatically disqualify you if you can explain the circumstances.

Debt-to-Income Ratio: The Hidden Approval Killer

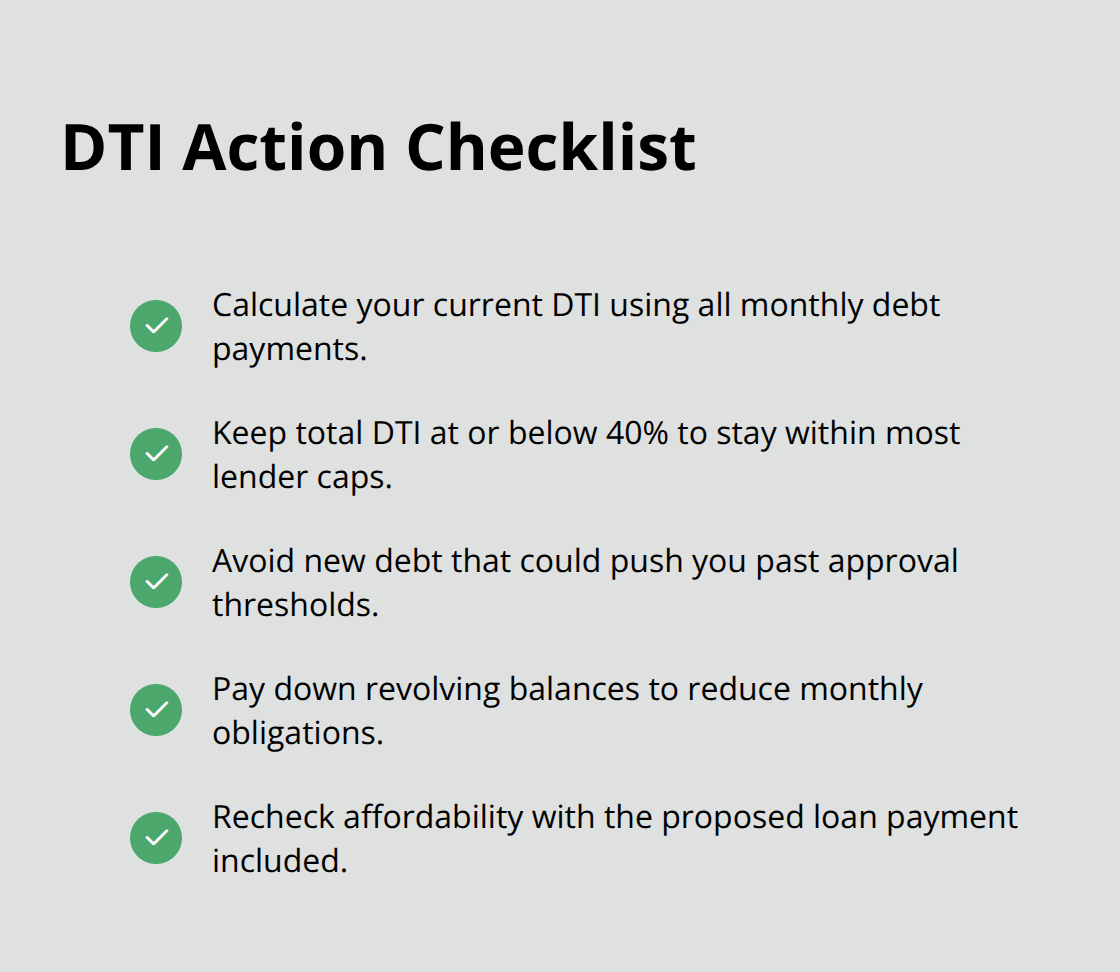

Your debt-to-income ratio is the metric that kills applications more often than credit score alone. If you earn $4,000 monthly and already carry $1,500 in monthly debt payments (mortgage, car loan, credit cards), your debt-to-income ratio sits at 37.5%, and most lenders cap approvals at 40–45%. That $10,000 personal loan with a $200 monthly payment could push you past that threshold and trigger a decline, even with a 700+ credit score.

Calculate your total monthly debt obligations before applying and be honest about what you can actually afford. If your ratio exceeds 40%, focus on paying down existing debt first rather than adding another loan, because lenders will offer you higher rates to compensate for the risk, making the borrowing more expensive overall. This approach protects your financial health and improves your odds of approval at better rates when you do apply.

Final Thoughts

Pull your credit report from Equifax Canada or TransUnion Canada and dispute any errors you find-this single step takes 30–45 days but often improves your approval odds and the rates you’ll receive. Calculate your debt-to-income ratio by dividing your total monthly debt payments by your gross monthly income, and if that number exceeds 40%, focus on paying down existing debt rather than adding a new loan. Gather your income documentation now so you accelerate the approval process when you apply.

Use online comparison tools to collect written quotes from at least three lenders without hard inquiries damaging your score. Input your desired loan amount, term, and credit range into platforms like Ratehub.ca and compare the APR, monthly payment, total cost, and prepayment policies across each offer. This comparison reveals which lender actually saves you money, not just which advertises the lowest rate.

The right loan for your situation depends on your specific needs and financial capacity-a personal loan works for home renovations or debt consolidation, an auto loan suits vehicle purchases, and a secured line of credit makes sense for large ongoing expenses. We at Financial Canadian help you navigate your borrowing options through practical guides and rate comparisons, and we believe the same principle applies to your financial strategy: a well-designed approach beats rushing into the first offer you receive. Take time to compare, verify your eligibility, and choose the loan that fits your budget and timeline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment