Personal loans can help you cover major expenses, but the interest rate you qualify for makes a huge difference in what you’ll actually pay back. Canada personal loan rates vary significantly depending on your financial profile and which lender you choose.

At Financial Canadian, we’ve put together this guide to help you understand what lenders look at and how to compare your options side by side. The right comparison strategy can save you hundreds or even thousands of dollars.

What Really Affects Your Personal Loan Rate

Your credit score is the single most important factor lenders examine, but it’s not the only one. Lenders across Canada typically view credit scores of 580 to 660 as acceptable for personal loans, though your exact rate depends on where you fall within that range. According to Ratehub data from February 2026, major banks like Scotiabank advertise rates starting at 6% for well-qualified borrowers, while those with weaker credit may face rates between 15% and 35% APR. The difference between a score of 660 (good range) and 760 (excellent range) can easily cost you thousands of dollars over the life of a loan. Your payment history matters most-one missed payment can damage your score for years, while consistent on-time payments gradually improve your profile. Check your actual credit report through Equifax Canada or TransUnion Canada before applying anywhere; errors on your reports can artificially lower your scores and qualification rates.

Your Credit Score Determines Your Starting Point

Lenders weight your credit score heavily because it reflects your past borrowing behavior. A higher score signals that you’ve managed debt responsibly, which translates to lower interest rates. Scores between 660 and 724 fall into the “good” range, while scores from 725 to 759 qualify as “very good,” and anything from 760 to 900 reaches “excellent” status. Each tier typically unlocks better rates from lenders. Scores below 600 make qualification difficult, though secured loans (backed by collateral) can still be an option. Your payment history accounts for about 35% of your score, so late payments or defaults have outsized impact on your borrowing costs.

Income and Employment Stability Shape Your Qualification

Lenders want proof that you can actually repay what you borrow, which is why they scrutinize your income and job history. Salaried employees with stable, long-term employment typically qualify for better rates than contract workers or those with gaps in employment. You’ll need to provide recent pay stubs, tax returns, and employment verification when you apply. Avoid changing jobs immediately before applying for a loan, as lenders view employment stability as a sign of reliable income.

Your Debt-to-Income Ratio Affects Your Rate More Than You Realize

Your debt-to-income ratio-the percentage of your monthly income that goes toward existing debts-is equally critical to lenders. If you’re already carrying significant credit card balances or other loans, lenders see you as riskier and charge higher rates accordingly. Calculate your total monthly debt payments and divide by your gross monthly income; if that number exceeds 40%, most lenders will either deny you or offer unfavorable terms. The good news is that this metric is something you can improve before applying by paying down existing balances. Even reducing credit card debt by 20% can meaningfully improve your debt-to-income ratio and your loan qualification rate.

What Lenders Actually See When They Pull Your File

When you apply for a personal loan, lenders conduct a hard credit inquiry that pulls your complete credit history and current balances. This inquiry may cause a small temporary dip in your score, but the impact fades within a few months. Lenders also verify your employment status through phone calls or documentation and cross-reference your stated income against tax records.

They examine the types of credit you hold (credit cards, car loans, mortgages) and how long you’ve maintained each account. Older accounts in good standing work in your favor, while recent collections or charge-offs work against you. Understanding what lenders see helps you identify which factors you can improve before shopping for rates.

Key Factors to Compare When Shopping for Personal Loans

The interest rate you’re quoted is only part of the story. When Ratehub analyzed personal loan offerings across Canada in February 2026, they found that APR ranges from 6% to 35%, with major banks like Scotiabank starting at 6%, BMO between 8.99% and 22.99%, TD between 8.99% and 23.99%, CIBC between 9% and 10%, and RBC between 9% and 13%. The advertised rate applies to well-qualified borrowers, not necessarily to you. The actual cost of your loan depends on three factors most people overlook: origination fees, prepayment penalties, and variable-rate structures.

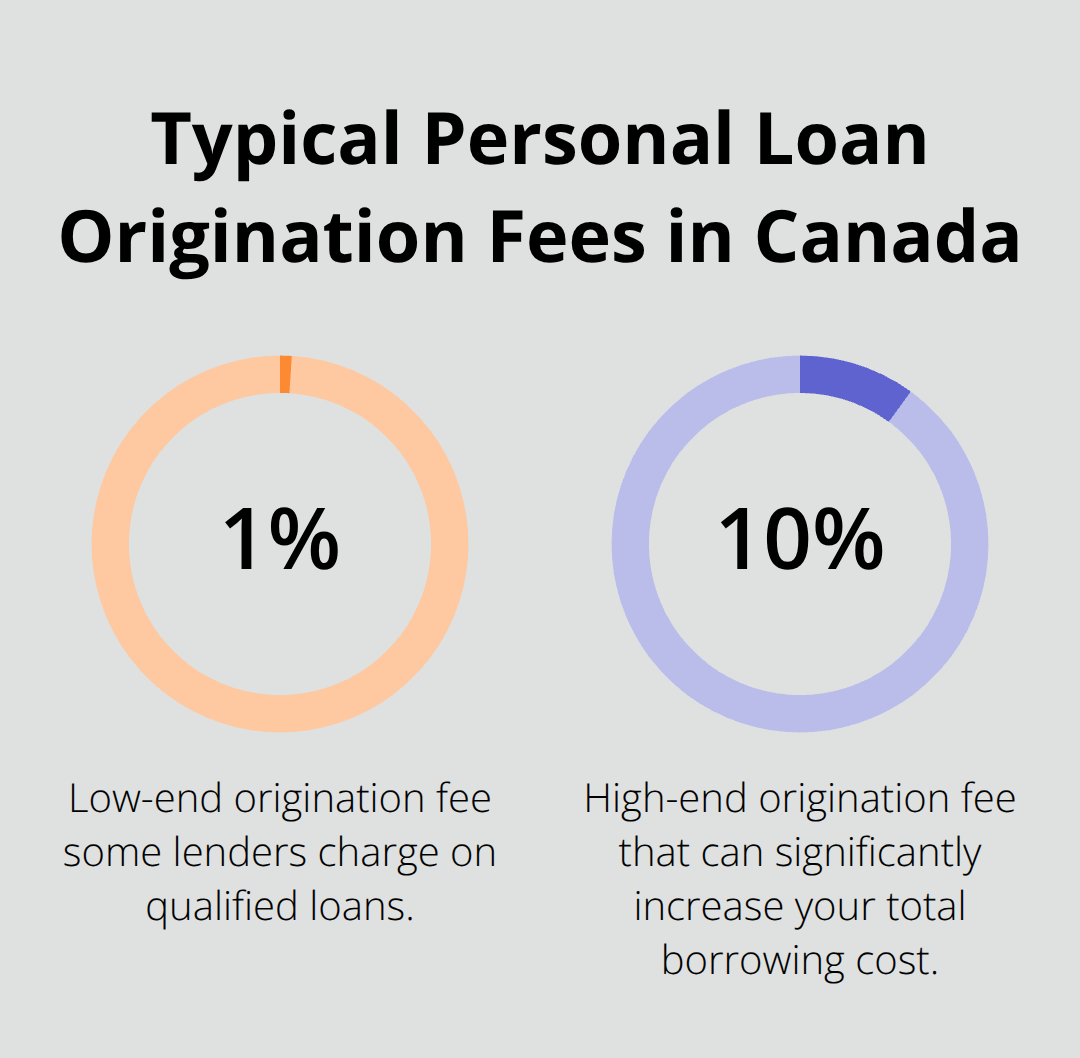

Origination Fees and Hidden Costs Add Up Fast

Origination fees typically range from 1% to 10% of the loan amount. On a $5,000 personal loan, this means you’ll pay an extra $50 to $500 before you even receive the money. Some lenders reduce the cash you receive; others add the fee to your loan balance. Either way, these costs increase your total borrowing expense significantly.

Late payment fees and other charges compound the problem if you miss a payment or pay late. Always ask lenders to disclose all fees upfront and calculate them into your total cost comparison.

Fixed Rates Versus Variable Rates Change Your Payment Risk

Fixed-rate loans keep your payment stable regardless of what the Bank of Canada does, while variable-rate loans move with the prime rate, which held at 2.25% as of April 29, 2026. If rates rise, your payment increases; if they fall, you save money. Variable-rate loans offer lower initial rates but expose you to payment uncertainty. Fixed-rate loans cost more upfront but provide payment predictability. Your choice depends on whether you value stability or want to gamble on rate decreases.

Loan Terms Dramatically Affect Your Total Interest Cost

Loan terms in Canada typically run from six months to five years, but longer terms lower your monthly payment while increasing total interest paid significantly. A $10,000 loan at 12% APR costs $2,156 in interest over five years but only $636 over two years, yet your monthly payment drops from $222 to $438 respectively. For a typical $5,000 personal loan at rates between 10% and 20% APR, the difference between a 10% rate and a 20% rate on a five-year term means you’ll pay roughly $1,375 more in interest alone. Calculate the total cost of the loan over its entire term before deciding. Use loan calculators to estimate what you’ll actually pay in monthly installments plus all fees combined.

Secured Loans Offer Lower Rates but Real Risk

Secured loans backed by collateral like a car or home equity typically offer 2% to 4% lower rates than unsecured loans because the lender can recoup losses by seizing the asset. This security comes with real risk: default on a secured personal loan and you lose your collateral. Unsecured loans don’t require collateral but may carry higher interest rates and stricter credit requirements; they can offer faster approvals and less paperwork. Weigh the rate savings against the risk of losing your asset if you hit financial trouble.

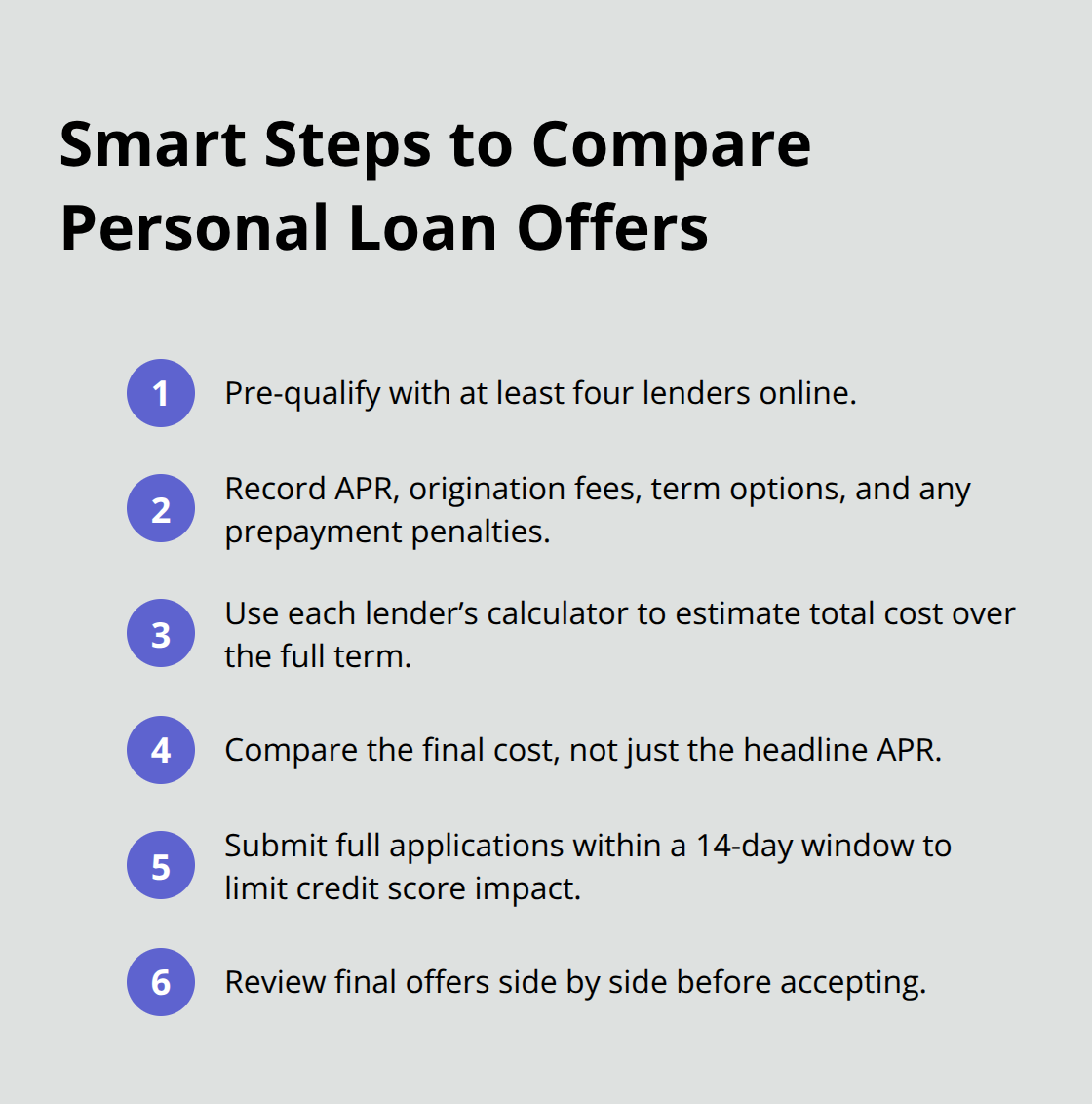

Pre-Qualify Across Multiple Lenders Before Applying

Pre-qualify with several lenders to view APRs without hard credit pulls, then compare the total cost, prepayment options, and any penalties before submitting a full application. This approach lets you shop around without damaging your credit score multiple times. Prepayment penalties can trap you into paying interest longer than necessary if you want to pay off the loan early, so confirm whether your lender allows early repayment without penalty. Understanding these comparison points positions you to evaluate where to actually borrow.

Where to Borrow for the Best Rates

Canada’s lending landscape has fragmented dramatically over the past five years, and that fragmentation works in your favor. The Big Six banks-RBC, TD, BMO, Scotiabank, CIBC, and National Bank-still dominate personal lending, but they’re no longer your only option. Major banks advertise competitive starting rates: Scotiabank at 6%, CIBC between 9% and 10%, RBC between 9% and 13%, while BMO and TD range from 8.99% to 22.99%. However, these advertised rates apply only to borrowers with excellent credit, typically 760 or higher. If your score sits between 660 and 759, you’ll qualify for rates significantly higher than what banks advertise. The real advantage of traditional banks is stability and regulatory oversight; they won’t disappear overnight, and their loan terms are standardized and transparent.

Banks Move Slowly but Offer Stability

Traditional banks require extensive documentation and take longer to approve applications than online alternatives. This slower pace reflects their rigorous underwriting process, which protects both the lender and borrower through standardized terms. Banks conduct thorough employment verification and cross-reference your income against tax records before committing funds. If you have a score above 720 and can wait a week for approval, banks offer the best rates available in Canada’s market.

Online Lenders and Fintechs Prioritize Speed

Online lenders and fintech companies like Spring Financial, goPeer, Mogo, and Fig Financial have captured market share specifically because they process applications faster and approve borrowers banks reject. These platforms typically charge higher rates-sometimes 15% to 35% APR-but they excel at serving people with fair credit scores between 600 and 660. Online lenders also offer more flexible terms and smaller loan minimums, making them ideal if you need less than $5,000 or want approval within 24 hours. The trade-off is clear: you sacrifice rate competitiveness for speed and accessibility.

Credit Unions Offer Middle Ground

Credit unions sit between banks and online lenders in terms of rates and approval speed; they often offer personalized service and slightly lower rates than major banks for members with a decent credit score. Their lending criteria and rates vary widely by institution, so contact your local credit union to ask about specific lending programs for lower-credit borrowers. Credit unions frequently provide more flexibility than banks while maintaining lower rates than online platforms.

Compare Across Multiple Lenders Strategically

Your choice depends on three factors: how quickly you need money, what your credit score actually qualifies for, and whether you prioritize the lowest possible rate or the fastest approval. If your score is between 650 and 720, compare both banks and online lenders because some fintechs will beat bank rates for this middle tier. If your score is below 650, online lenders become your realistic option, though you should still contact local credit unions to ask about their specific lending programs.

Contact at least four lenders-two banks and two online platforms-and request pre-qualification estimates without hard credit pulls. Most lenders now offer this service through their websites within minutes. Write down the exact APR, origination fees, term options, and any prepayment penalties each lender quotes you. Calculate the total cost of borrowing $5,000 at each quoted rate over a three-year term using their loan calculators, then compare the final numbers rather than the advertised rates. A lender quoting 10% APR might cost less overall than one quoting 8% if the first charges no origination fee while the second charges 5%.

Once you’ve narrowed your choices to two or three lenders, submit full applications. Hard pulls from multiple lenders within a 14-day window count as a single inquiry for credit scoring purposes, so don’t space out applications over weeks. This timing strategy protects your credit score while letting you shop aggressively. After approval, you have a window-typically 30 days-to accept or decline the offer without obligation, giving you time to compare final terms side by side before committing.

Final Thoughts

Shopping for a personal loan requires comparing more than just the advertised interest rate. Your Canada personal loan rates depend on your credit score, income stability, and debt-to-income ratio, but the lender you choose matters equally. Before applying anywhere, pull your credit reports from Equifax Canada or TransUnion Canada to verify your actual score and identify any errors that could artificially lower your qualification rates. When you’re ready to compare offers, focus on total cost rather than the headline APR.

Calculate what you’ll actually pay in interest plus origination fees over the full loan term using each lender’s calculator. A loan advertised at 8% with a 5% origination fee costs more than one at 10% with no fees. Request pre-qualification estimates from at least four lenders without hard credit pulls, then submit full applications within a 14-day window so multiple inquiries count as a single credit check. Paying down existing credit card balances before applying can improve your debt-to-income ratio and unlock better rates.

The difference between a 10% rate and a 20% rate on a five-year personal loan can cost you thousands of dollars. That’s why taking time to compare across multiple lenders before committing matters. We at Financial Canadian help you navigate financial decisions with clear information and practical guidance-explore our resources to strengthen your borrowing strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment