Your credit score shapes your financial life in Canada. It determines whether you qualify for loans, what interest rates you’ll pay, and how lenders perceive your reliability.

At Financial Canadian, we’ve created this credit score Canada guide to show you exactly how to build and protect your rating. The steps are straightforward, and the payoff is significant.

How Your Credit Score Really Works in Canada

Your credit score is a three-digit number that lenders use to predict whether you’ll repay borrowed money. In Canada, scores range from 300 to 900, with higher numbers indicating lower risk. Equifax Canada and TransUnion Canada are the two major credit bureaus that calculate and report these scores. Each bureau uses multiple scoring models, which explains why your score from Equifax might differ from your TransUnion score-and that’s completely normal.

The Five Factors That Shape Your Score

Payment history accounts for roughly 35% of your score. Missed or late payments damage your rating far more than other mistakes. Credit utilization, the ratio of what you owe to your available credit limits, makes up about 30% of your score. The Financial Consumer Agency of Canada recommends keeping this ratio under 30%, though lower is always better.

Length of credit history contributes around 15%, credit mix about 10%, and recent inquiries another 10%. Hard inquiries-those made when you apply for credit-can temporarily lower your score, especially if you rack up multiple applications in a short timeframe. Soft inquiries, like when you check your own score or a lender pre-approves you for an offer, don’t affect your rating at all.

How Your Score Opens or Closes Financial Doors

Lenders pull your credit report before approving mortgages, auto loans, credit cards, and rental applications. A score above 700 is generally considered good across most Canadian lenders, though some will work with lower scores at higher interest rates. The difference in interest rates between a 650 score and a 750 score can cost you thousands over a mortgage term. A borrower with a lower score might pay 0.5% to 1.5% more in interest on a $400,000 mortgage, which translates to roughly $20,000 to $60,000 in additional costs over 25 years.

Beyond loans, landlords increasingly check credit scores before renting apartments, employers in certain sectors review them, and utility companies may require deposits based on your rating. Your score also affects insurance premiums in some provinces. The higher your score, the more favorable terms you’ll receive across nearly every financial product available to you.

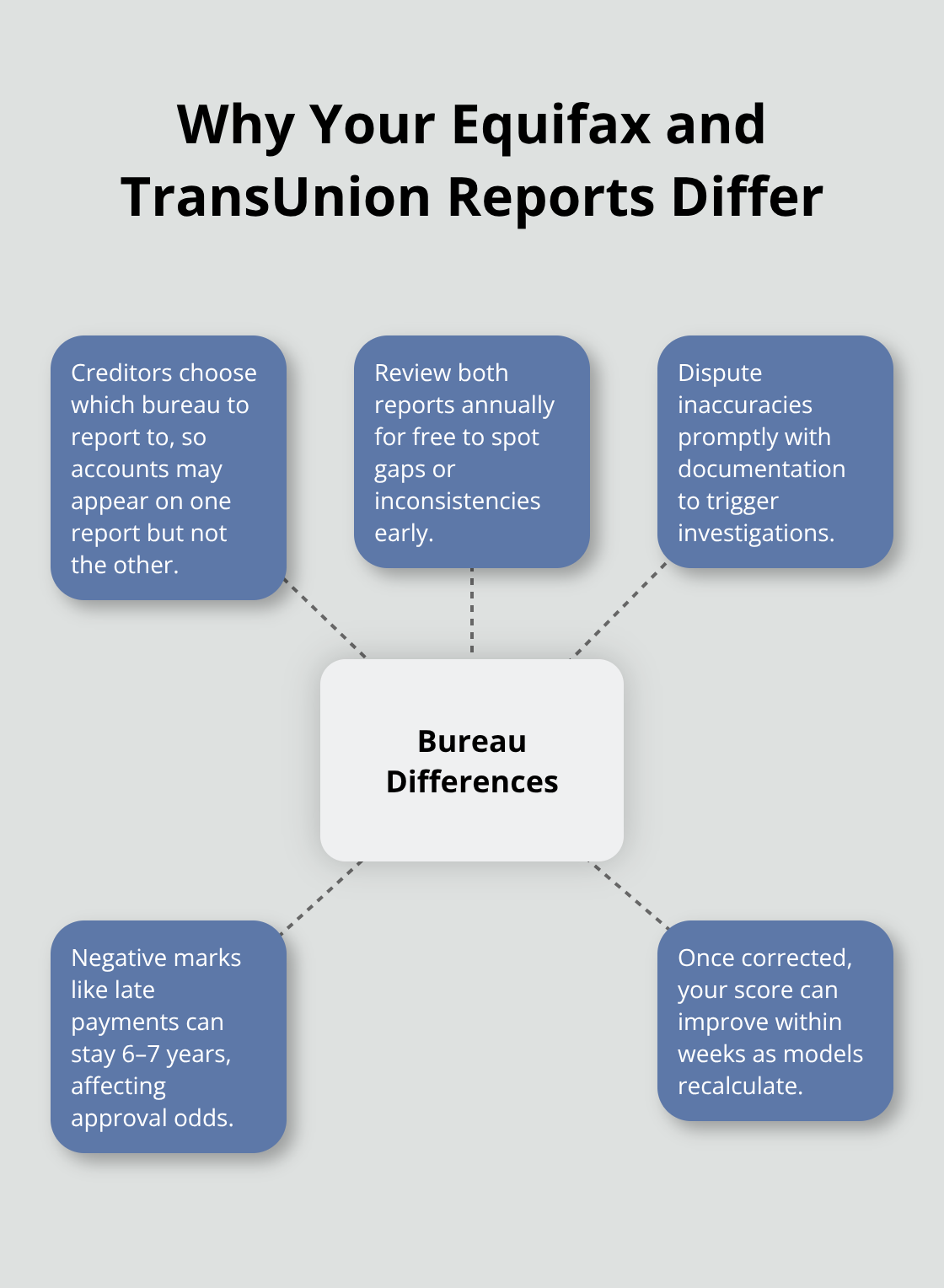

Why Equifax and TransUnion Report Different Information

Equifax Canada and TransUnion Canada don’t always report identical information because creditors choose which bureau to report to. A credit card issuer might report to TransUnion but not Equifax, creating gaps in your file at each bureau. This is why checking your credit report from both bureaus annually-which is free-matters significantly. You can request free reports directly from each bureau’s website.

When you spot errors like a missed payment that wasn’t actually missed or an account that isn’t yours, dispute it immediately with the bureau. Corrected information can raise your score within weeks. Late payments typically remain on your file for 6 to 7 years, bankruptcies for about 7 years after discharge, so timing and accuracy are critical to your long-term financial health. Understanding these differences between bureaus sets the stage for the practical steps you can take to build and improve your rating.

How to Actually Improve Your Credit Score

Master Payment History and Credit Utilization First

The most effective way to raise your credit score is to attack the two factors that control 65% of your rating: payment history and credit utilization. Payment history accounts for 35% of your score, which means a single missed payment can set you back months of progress. The Financial Consumer Agency of Canada recommends setting up automatic payments for at least your minimum balance on every account you hold. This single habit eliminates the risk of forgetting a due date entirely.

If you can afford it, pay your full balance each month to avoid interest charges and keep your utilization ratio at zero for that account. Many people assume they need to carry a balance to build credit, but that’s false. Lenders care whether you pay on time, not whether you pay interest.

Lower Your Credit Utilization Ratio Strategically

Credit utilization is the second lever you control immediately. This ratio measures how much of your available credit you currently use, and keeping it under 30% has a measurable impact on your score. If you have a credit card with a $5,000 limit, try to keep your balance below $1,500 at all times. The gap between 30% utilization and 10% utilization is significant enough to affect your approval odds for major loans like mortgages.

One practical tactic is to request credit limit increases from your existing card issuers without applying for new cards. A higher limit automatically lowers your utilization ratio without adding a hard inquiry to your file. You can also split your spending across multiple cards to distribute your utilization, though this only works if you stay disciplined about tracking payments across accounts.

Fix Errors on Your Credit Report Immediately

If errors appear on your credit report from Equifax Canada or TransUnion Canada, dispute errors directly with the bureau that reported the mistake. Provide documentation showing the error, and the bureau must investigate within 30 days. Corrected information can raise your score within weeks because the error is removed from the calculation immediately.

Build Credit Mix Strategically

Building credit mix-holding different types of credit like installment loans and revolving credit-matters less than the first two factors, but it does contribute roughly 10% to your score. Only pursue new credit types if you actually need them, not to artificially boost this category. Opening accounts you don’t need creates hard inquiries that temporarily lower your score and increase your overall debt obligations. The mistakes you make during this phase of building your score can take years to recover from, which is why the next chapter focuses on the specific errors that damage your rating most severely.

Mistakes That Tank Your Credit Score

Late Payments Destroy Your Score Fast

A single missed payment causes far more damage than most people realize. Payment history accounts for 35% of your credit score, meaning one missed payment can erase months of progress. A payment that’s 30 days late stays on your credit report for 6 to 7 years, and the damage is immediate-your score can drop 100 points or more from a single missed payment. The longer the delinquency, the worse the impact.

A 90-day late payment signals serious financial trouble to lenders and will disqualify you from competitive mortgage rates for years. The solution is non-negotiable: set up automatic payments for at least your minimum balance on every account today. This eliminates the excuse of forgetting a due date entirely. If you miss a payment, contact your creditor within 30 days to discuss options before the account officially reports as late to the bureaus.

Maxing Out Credit Cards Signals Financial Stress

Credit utilization makes up 30% of your score, and carrying balances above 30% of your limits signals financial stress to lenders. If you have a $5,000 credit card limit and carry a $4,000 balance, you’re at 80% utilization-this single factor can lower your score by 50 to 100 points even if you pay on time. The damage compounds when you max out multiple cards simultaneously. Try to lower your credit card balances well below your limits at all times.

Closing Old Accounts Reduces Your Credit History Length

Your length of credit history contributes 15% to your score, and closing older accounts reduces your average account age, which lowers your rating. Keep old credit cards open and dormant rather than closing them. This strategy maintains the age of your credit file and protects your score from unnecessary damage.

Multiple Credit Applications in Short Periods Hurt Your Rating

Each credit application triggers a hard inquiry that temporarily lowers your score by 5 to 10 points, and multiple inquiries within 6 months signal desperation to lenders. If you need credit, space applications at least 6 months apart and apply only when you genuinely need new credit, not to artificially boost your credit mix percentage. This disciplined approach prevents the accumulation of hard inquiries that can take months to fade from your file.

Final Thoughts

Building a strong credit score in Canada requires consistent action across two core areas: paying bills on time and keeping credit utilization low. These two factors control 65% of your score, which means focusing here delivers the fastest results. Payment history alone accounts for 35%, so setting up automatic payments eliminates the single biggest threat to your rating, while credit utilization makes up another 30% and keeping balances under 30% of your limits signals financial responsibility to lenders.

The long-term strategy for protecting your score involves three habits that compound over time. Check your credit reports from both Equifax Canada and TransUnion Canada annually to catch errors before they damage your rating for years. Keep older credit accounts open even if you don’t use them regularly, since closing accounts reduces your average account age and lowers your score unnecessarily. Space any new credit applications at least six months apart to avoid accumulating hard inquiries that temporarily lower your rating.

Request your free credit reports from both bureaus today and review them for inaccuracies (this takes less than an hour but protects your financial future significantly). If you find errors, dispute them immediately with documentation. Then implement automatic payments for at least your minimum balance on every account you hold, and use this credit score Canada guide as your reference whenever you need to revisit these strategies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment