Personal loan rates in Canada are climbing, and most borrowers have no idea what they should actually expect to pay. At Financial Canadian, we’ve analyzed current rates across major lenders to show you exactly where the market stands right now.

Your credit score, the loan amount you need, and broader economic conditions all shape the rate you’ll qualify for. The good news is that you have more control over your rate than you might think.

Current Personal Loan Rates in Canada

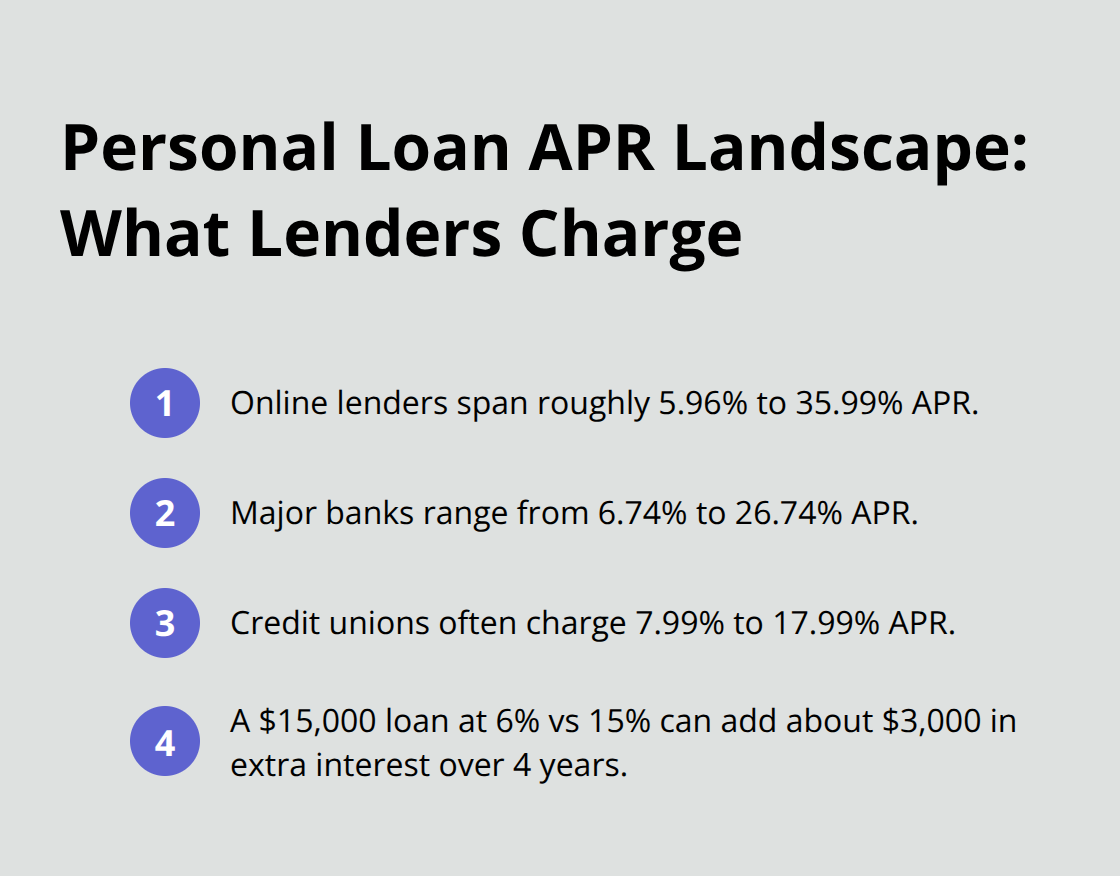

What Lenders Charge Right Now

The Bank of Canada held its policy rate at 4.25% through June 2026, having cut rates once in December 2025 but made no further moves this year. That stability at the central bank level masks real volatility in what lenders actually charge. As of June 2026, personal loan APRs from online lenders span roughly 5.96% to 35.99%-a spread so wide that your actual rate depends entirely on your financial profile. Major banks like Wells Fargo offer rates from 6.74% to 26.74%, while credit unions such as PenFed charge between 7.99% and 17.99%. The difference between the lowest and highest available rate matters enormously. A $15,000 loan at 6% versus 15% over four years adds roughly $3,000 in interest, so shopping around becomes essential if you want to avoid overpaying.

Where Your Credit Score Places You

Your credit score determines which part of that range applies to you. Borrowers with excellent credit (800+) qualify for rates around 15.75% APR on average, while those with good credit (670–739) face roughly 23.27% APR. Fair credit (580–669) pushes you toward 27.79% APR, and poor credit below 580 sits near higher rates. The gap between excellent and fair credit widens your costs substantially, making credit improvement a worthwhile priority before you apply. CIBC’s offerings illustrate what Canadian lenders provide: personal loans with fixed or variable rates tied to Prime, terms from one to five years, and rates that shift as the Bank of Canada’s policy rate decisions filter through the system.

How Loan Terms Affect Your Rate

Three-year loans average around 13.86% APR, while five-year loans climb to 17.52% APR as of late May 2026. The term you choose directly impacts your cost-shorter terms mean lower rates but higher monthly payments, while longer terms reduce your monthly burden at the expense of substantially more interest paid overall. A $10,000 loan over three years may incur roughly $1,032–$6,489 in interest, whereas the same loan over five years may cost roughly $1,737–$11,680 in interest. This difference compounds quickly, so you should calculate your actual monthly payment against your budget before locking in a longer term.

How 2026 Rates Compare to Recent History

Personal loan rates remain elevated compared to 2020–2021 when borrowing costs were near historic lows. The Federal Reserve Bank of St. Louis reported that the average APR on a 24-month personal loan from banks hit 11.40% in February 2026, well above the sub-10% rates borrowers enjoyed during the pandemic era. Lenders priced in higher risk and elevated funding costs, and those prices have stuck despite the Bank of Canada’s December rate cut. You cannot assume rates will drop meaningfully before year-end, so locking in a competitive rate now beats waiting for conditions that may never materialize.

Your Next Move: Prequalification Without Risk

Prequalification with multiple lenders reveals your actual options without a hard credit pull, letting you compare APRs, origination fees, and terms side by side before committing to an application. This step costs nothing and protects your credit score while you assess what different lenders will actually offer you. Once you understand where you stand, you can focus on what lenders actually look at when pricing your loan-and which ones you can control.

What Actually Controls Your Personal Loan Rate

Credit Score: Your Primary Rate Determinant

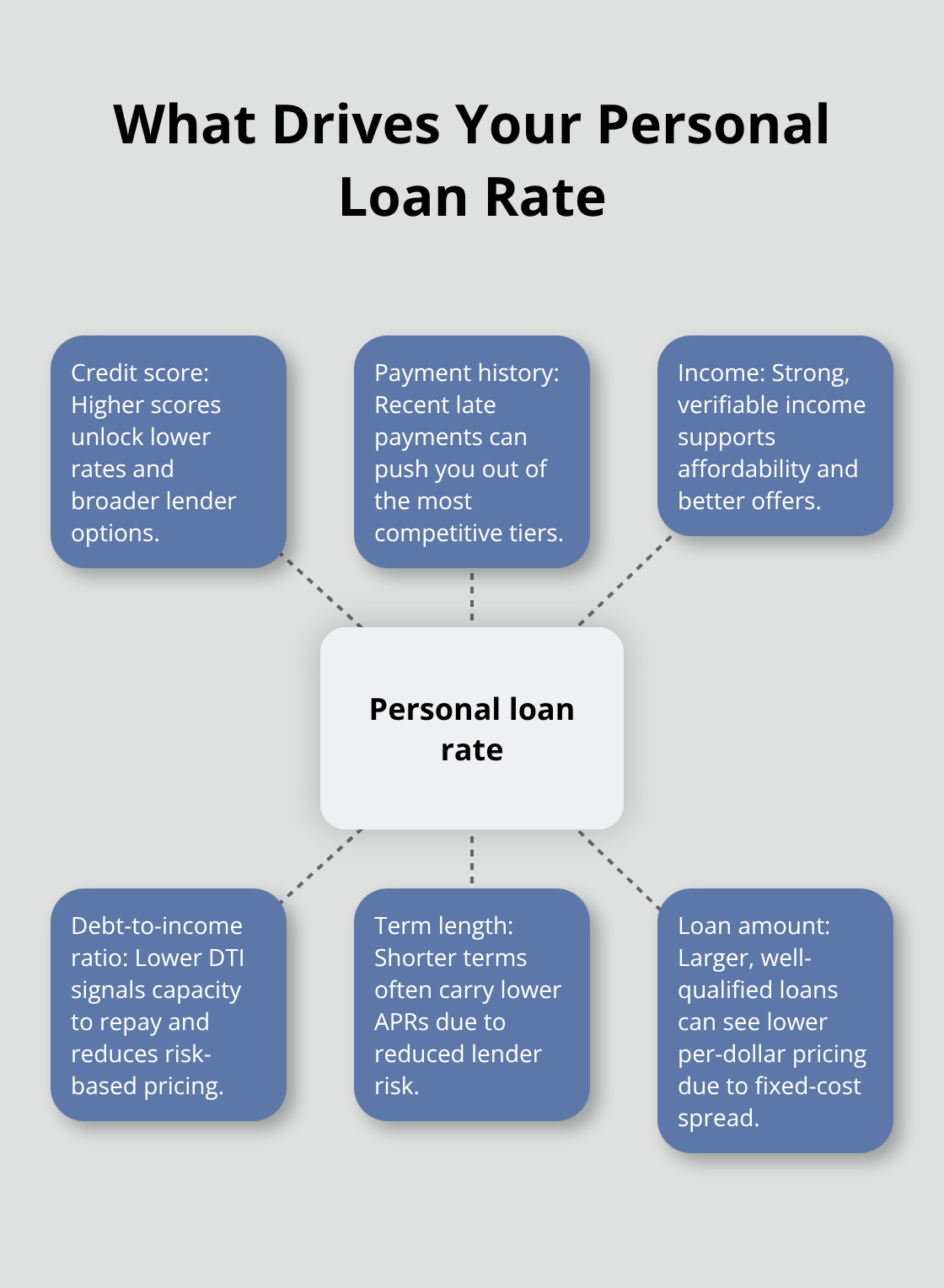

Your credit score acts as the primary gatekeeper for personal loan rates. Lenders assess four core factors when pricing your loan: credit score, payment history, income, and debt-to-income ratio.

Borrowers with scores above 740 consistently access rates in the low teens, while those between 670 and 739 face rates pushing into the low 20s. Below 670, you compete for lender attention in a much tighter market where rates routinely exceed 27%. The gap isn’t small change either. On a $10,000 loan, moving from a 720 score (roughly 14.48% APR) to a 650 score (roughly 22.89% APR) costs you an extra $800 to $1,200 in total interest depending on your term.

Payment history weighs heavily within that score. Even one missed payment can lock you out of competitive rates for months. Your debt-to-income ratio matters equally. If you carry $30,000 in existing debt on a $60,000 salary, lenders see you as overextended regardless of your credit score. Reduce existing debt before applying to move the needle faster than waiting for your score to climb naturally.

How Co-signers Lower Your Rate

A co-signer with strong credit and separate income can lower your rate substantially because lenders view you as lower risk when someone else guarantees the loan. Credit unions like PenFed and First Tech actively use co-signers to approve borrowers who wouldn’t qualify alone, often shaving 2% to 4% off standard rates. This strategy works because the lender gains a second income source and a backup repayment obligation.

Loan Term and Amount Shape Your Pricing

For customers with a 700 FICO score and $5,000 loan amount, three-year terms average 12.27% APR as of June 2026, a spread driven by lender risk calculations and funding costs. Shorter terms mean the lender recovers their money faster and faces less inflation risk, so they price that certainty into lower rates. Loan size also influences your offer. A $5,000 loan carries different pricing than a $50,000 loan because the fixed costs of origination and underwriting hit differently depending on the amount. Larger loans often qualify for better rates per dollar borrowed.

Economic Conditions and Lender Risk Appetite

Economic conditions filter through everything. The Bank of Canada’s policy rate sits at 4.25%, but that doesn’t translate directly to your personal loan rate. Instead, lenders watch inflation data, employment trends, and expectations about future central bank moves. When inflation stays elevated or the economy shows weakness, lenders widen their margins and push rates higher to compensate for perceived risk.

The Federal Reserve Bank of St. Louis data from February 2026 showed bank personal loan APRs at 11.40% for 24-month terms, yet online lenders quoted rates above 35% for the same period. That gap reflects lender business models and risk appetites, not market-wide conditions. Online lenders targeting borrowers with fair or poor credit price in higher default risk, while credit unions serving their membership base accept thinner margins. Your actual rate depends on which lender type you match with, which is why prequalifying with multiple lenders before applying reveals whether you’re getting a competitive offer or overpaying for convenience. Once you understand these rate drivers, you can move toward the practical steps that actually lower what you pay.

How to Lock In the Best Rate Before You Apply

Compare Offers Across Multiple Lenders

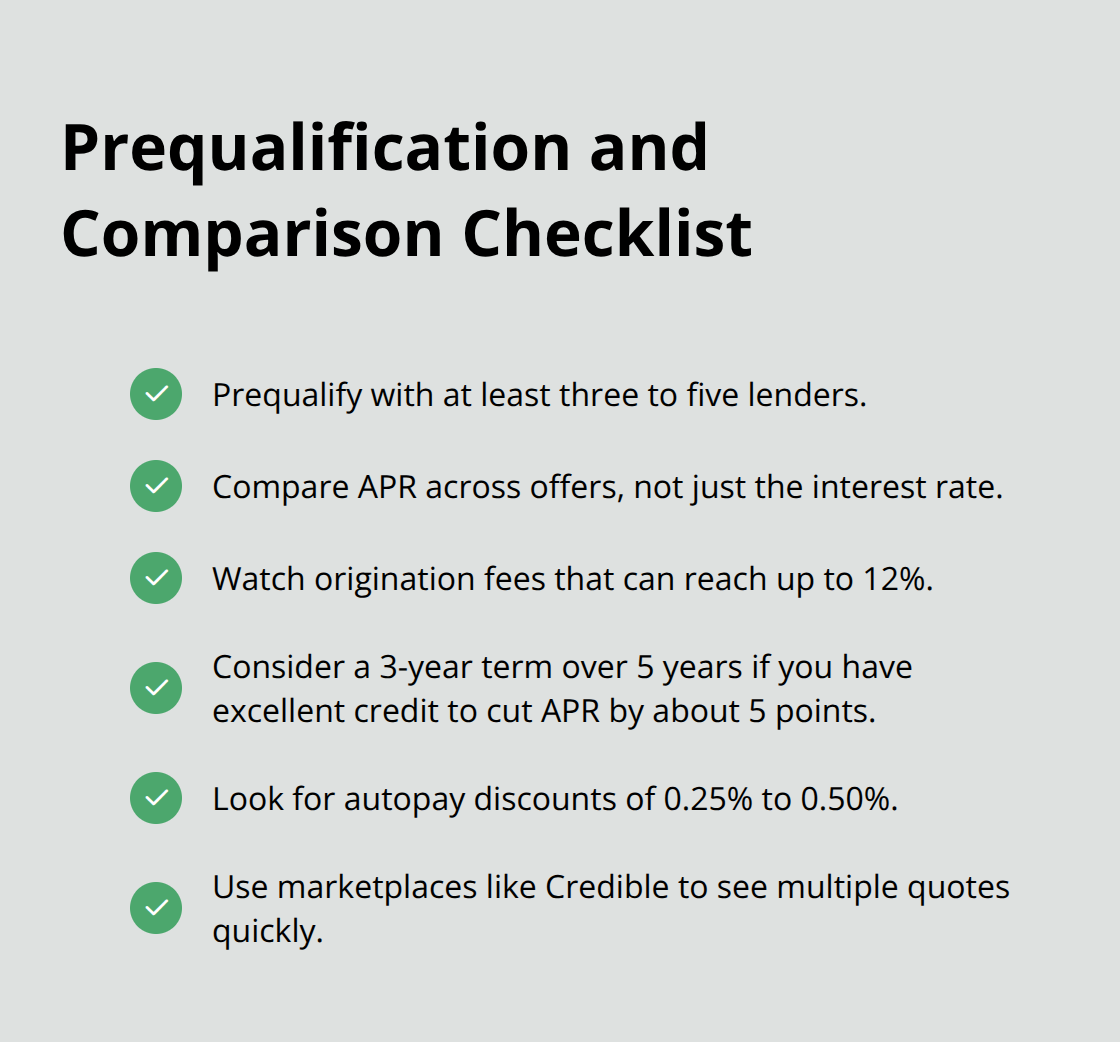

Compare offers from multiple lenders is the single most effective action you can take right now. Most borrowers submit one application to their bank and accept whatever rate they receive, leaving thousands of dollars on the table. A soft credit pull through prequalification costs nothing and reveals your actual options across different lender types without triggering a hard inquiry that damages your score. Online lenders, credit unions, and banks all price loans differently based on their risk models and target customer profiles.

When you prequalify with at least three to five lenders, you see the range of rates available to someone with your financial profile. Borrowers with excellent credit could reduce their APR by around 5 percentage points, on average, by choosing a 3-year over a 5-year term loan. Sites like Credible let you input your information once and receive quotes from multiple lenders instantly. Compare the APR, not just the interest rate, because origination fees up to 12% get buried in the APR figure. A lender quoting 9% interest with a 10% origination fee actually costs you more than one offering 10% interest with no fees. Many lenders also offer autopay discounts between 0.25% and 0.50%, so factor that into your comparison.

Reduce Your Debt-to-Income Ratio

Your credit score determines which part of the rate spectrum applies to you, but you have more control over this number than most borrowers realize. If your score sits below 700, spending 30 to 60 days improving it before applying can shift you into a meaningfully lower rate bracket. The fastest wins come from reducing your debt-to-income ratio through paying down existing balances, especially credit card debt. Lenders calculate DTI by dividing your total monthly debt payments by your gross monthly income. If you earn $5,000 monthly and carry $1,500 in debt payments, your DTI is 30%, which lenders view as acceptable. Push that to $2,000 in payments on the same income and you hit 40%, triggering rate penalties or outright rejections. Paying down even $200 to $300 in monthly obligations before applying moves the needle faster than waiting three to six months for score improvement through on-time payments alone.

Fix Credit Report Errors

Check your credit report at AnnualCreditReport.com before applying to catch errors that could be dragging your score down. Fix credit report errors immediately because lenders pull your report when pricing your loan, and errors cost you real money in higher rates. Correcting these errors takes weeks but costs nothing and directly improves your negotiating position with lenders.

Use a Co-signer to Lower Your Rate

For borrowers with fair or poor credit, adding a co-signer with strong credit and separate income dramatically improves your odds of approval and locks in lower rates. Credit unions like PenFed and First Tech actively structure loans around co-signers, often reducing rates by 2% to 4% compared to what you would qualify for alone. A co-signer does not need to put up collateral, but they do guarantee the loan if you miss payments, so choose someone you trust and ensure they understand the obligation. This approach works because the lender gains a second income source and secondary repayment responsibility, reducing their perceived risk.

Final Thoughts

Personal loan rates in Canada right now demand action, not waiting. The Bank of Canada’s policy rate sits at 4.25%, but that stability masks real variation in what lenders charge-borrowers with excellent credit access rates around 15.75% APR while those with fair credit face 27.79% APR on the same loan products. That gap represents thousands of dollars in unnecessary interest if you don’t shop strategically.

Your immediate priority is prequalification with at least three to five lenders to reveal your actual options without damaging your score. Compare APRs across banks, credit unions, and online lenders because each prices loans differently based on their risk models, and a 2% difference in APR on a $15,000 loan over four years costs you roughly $1,200 in extra interest. Before you apply formally, reduce your debt-to-income ratio by paying down existing balances, check your credit report at AnnualCreditReport.com for errors, and consider adding a co-signer with strong credit if your score sits below 700 (this step can reduce your rate by 2% to 4%).

Monitor the Bank of Canada’s policy decisions throughout 2026 because rate changes filter through to lender pricing within weeks, and current personal loan rates in Canada remain elevated compared to 2020–2021. Visit Financial Canadian to access tools and guidance tailored to your borrowing needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment