Buying a home in Canada moves faster when you’re preapproved. A mortgage preapproval letter signals to sellers that you’re a serious buyer with financing backing, giving you a real advantage in competitive markets.

At Financial Canadian, we’ve seen how understanding the Canada mortgage preapproval steps transforms the entire home-buying experience. This guide walks you through each stage so you can close on your new home with confidence and speed.

What Preapproval Actually Does for Your Home Purchase

A mortgage preapproval is a lender’s written commitment that you can borrow up to a specific amount based on your financial profile. The Financial Consumer Agency of Canada defines it as a detailed evaluation where the lender reviews your income, credit, debts, and down payment to determine your maximum borrowing capacity. This differs fundamentally from prequalification, which is a quick estimate without underwriting and carries minimal weight with sellers. Prequalification takes minutes and uses a soft credit check that doesn’t impact your score, while preapproval involves a hard credit check and thorough document review, typically taking two to three business days. According to Equifax, the hard check may lower your credit score by a few points, but scores usually recover within months. Most preapprovals remain valid for 90 to 120 days, giving you a concrete window to shop and make offers with confidence.

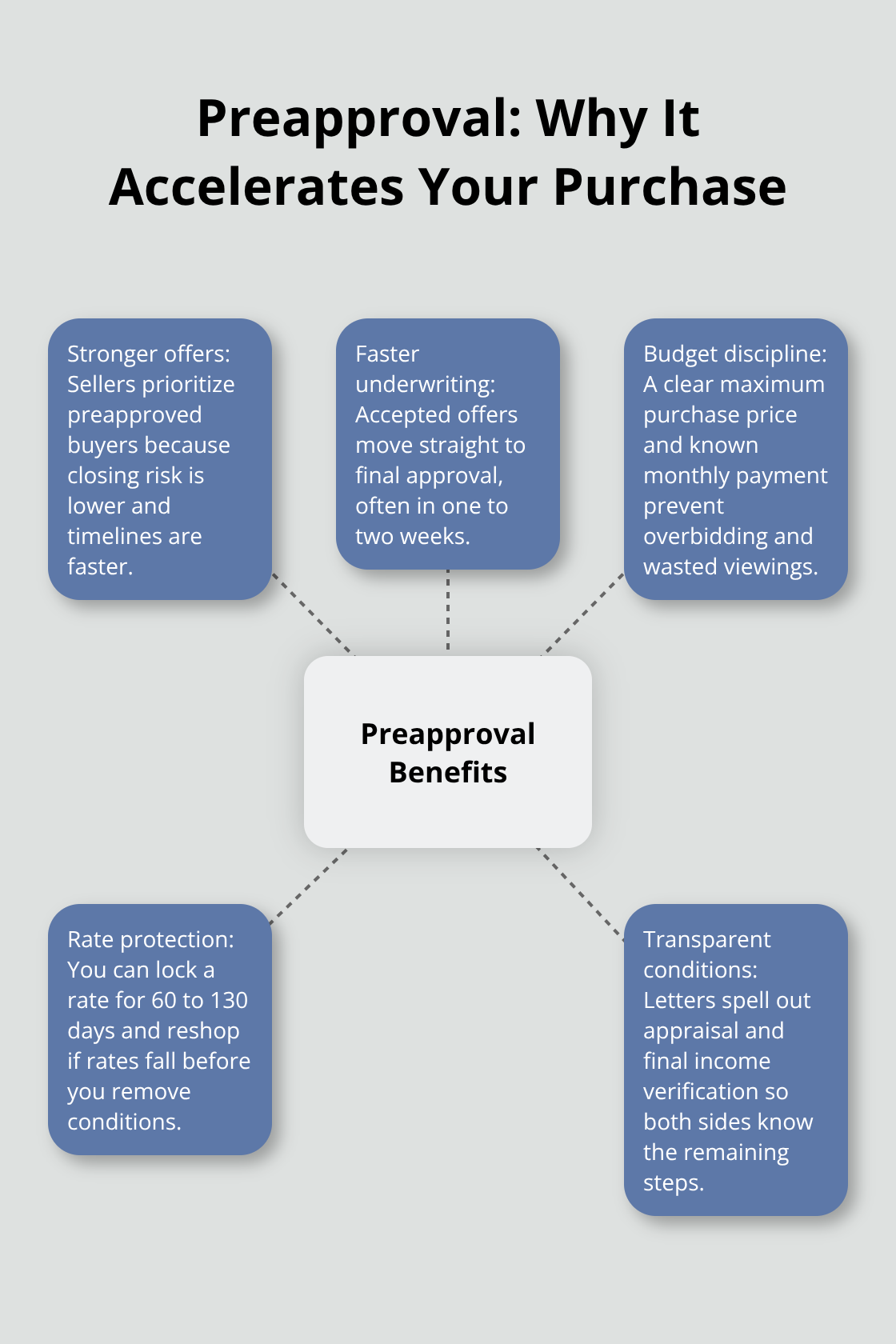

Why Sellers Take Preapproved Offers Seriously

When you submit an offer with a preapproval letter, you tell the seller your financing is verified and underwritten. Sellers in competitive markets prioritize offers backed by preapproval because it signals lower closing risk and faster transaction timelines. An accepted offer moves immediately to final approval, which typically takes one to two weeks after submission, whereas buyers without preapproval often face delays while lenders conduct initial underwriting. Your preapproval letter includes specific conditions tied to property appraisal and final income verification, meaning the seller knows exactly what hurdles remain. If your down payment is less than 20%, mortgage loan insurance from CMHC becomes part of your approval and is already factored into your preapproved amount. This clarity strengthens your negotiating position because sellers understand you won’t face surprise financing gaps.

How Your Budget Becomes Your Competitive Edge

Preapproval forces you to operate within a realistic budget before you start viewing homes. The Financial Consumer Agency of Canada notes that establishing a clear maximum purchase price prevents emotional overbidding and keeps you disciplined in competitive situations. Knowing your exact monthly payment, stress test obligations, and closing costs upfront means you won’t waste time on properties outside your reach. You can also lock an interest rate for 60 to 130 days during preapproval, protecting you from rate increases while you search. If rates fall during your rate hold, you can reshop your file to capture lower pricing before you remove conditions. This rate protection is a genuine financial advantage that prequalified buyers lack entirely.

Moving Forward with Your Preapproval Advantage

With your preapproval in hand, you now possess the documentation and financial clarity that accelerates every step ahead. The next phase involves using this letter strategically to find the right property and negotiate timelines that work in your favor.

How to Get Your Mortgage Preapproval in Canada

Prepare Your Documents Before You Apply

Incomplete applications cause the longest delays in the preapproval process. Your lender or mortgage broker may ask you to provide recent financial statements from bank accounts or investments. Start by downloading a document checklist from your lender’s website and organize everything in a single folder before you submit your application. This upfront work eliminates the most common reason preapprovals stall: missing paperwork. One missing document triggers back-and-forth emails that stretch the timeline unnecessarily.

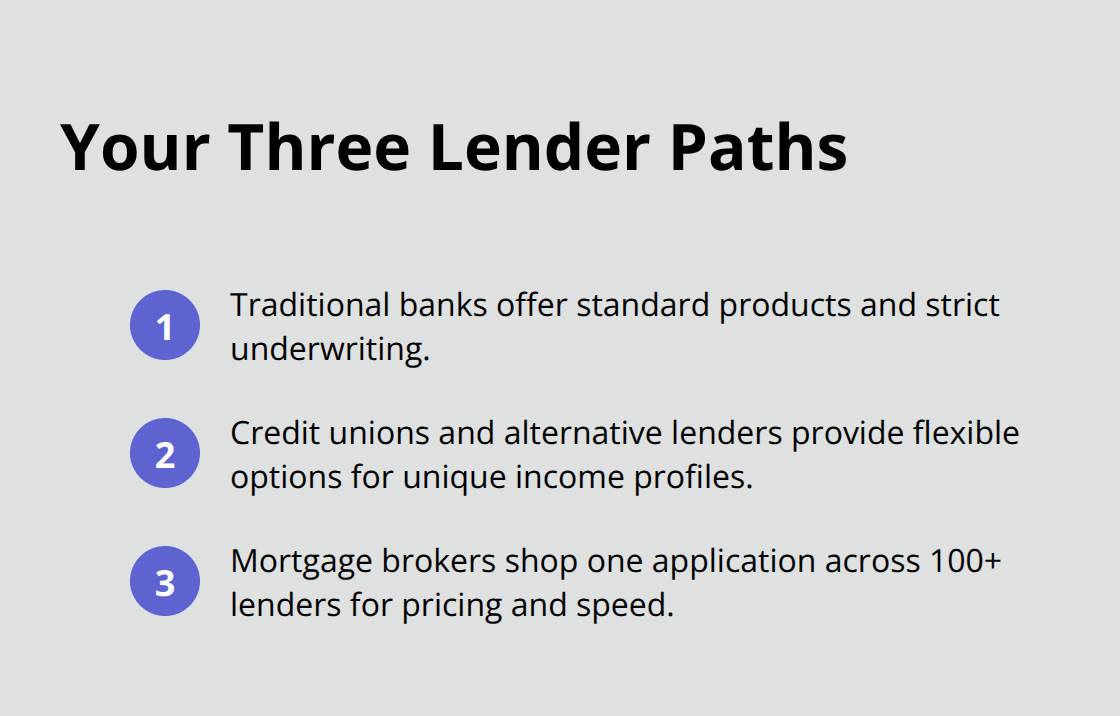

Choose Your Lender Strategically

You have three main paths: traditional banks, credit unions, or mortgage brokers who shop your file across multiple lenders. Many Canadians apply to only one bank, which limits their options significantly. If a traditional bank declines you, credit unions and alternative lenders often have more flexible programs for self-employed buyers, new Canadians, or those with non-traditional income.

A broker’s advantage is substantial. They submit your application once and compare rates across 100+ lenders, saving you time and typically securing better pricing and terms than shopping solo. Most brokers and lenders now accept online applications with secure document uploads, which accelerates the initial review stage considerably.

Navigate the Underwriting Phase

During underwriting, the lender verifies your employment, pulls your credit report using a hard inquiry that may impact your credit score, and confirms your down payment funds are legitimate and available. Appraisals are not ordered at this stage-that happens after you have an accepted offer.

Understand Your Preapproval Letter

After underwriting, you receive your preapproval letter, which states your maximum borrowing amount, applicable interest rate, and specific conditions like property appraisal and final income verification. This letter remains valid for 90 to 120 days, so check the expiration date and plan your house hunting timeline accordingly. If rates fall during your rate hold period, contact your lender immediately to reshop your file and capture the lower rate before you remove conditions on an offer.

The preapproval letter itself costs nothing; prequalification and preapproval are generally free services. Your rate depends on factors like your credit score, home equity, and the specific lender’s pricing, so the advertised rates you see online are typical benchmarks rather than guaranteed offers.

Move Forward with Your Preapproval in Hand

Once your preapproval letter arrives, you possess the documentation and financial clarity that accelerates every step ahead. With this letter in hand, you can now start house hunting with confidence and begin negotiating timelines that work in your favor.

Accelerate Your Closing After Preapproval

Deploy Your Preapproval Letter as Your Negotiating Weapon

Your preapproval letter is now your most valuable negotiating tool, and how you use it determines whether your closing happens in weeks or months. Start viewing properties immediately after you receive that letter. Sellers respond faster to preapproved offers, and the Financial Consumer Agency of Canada confirms that preapproval significantly reduces closing delays compared to buyers without one. Set a strict viewing schedule and commit to making an offer within two weeks of receiving your preapproval. Properties in competitive markets move quickly, and hesitation costs you opportunities.

Before you begin viewings, confirm your rate lock expiration date with your lender and calculate your exact maximum purchase price minus closing costs, which typically range from 1.5% to 4% of the home price. This precision prevents emotional bidding and keeps negotiations grounded in reality.

Submit Your Offer with Speed and Clarity

When you find a property you want, submit your offer immediately with your preapproval letter attached and explicitly state that you’re ready to close within 30 days. Sellers view 30-day closings as low-risk transactions compared to 45 or 60-day timelines, and this competitive advantage often wins offers in multiple-bid situations. Your preapproval letter signals to the seller that your financing is verified and underwritten, which reduces closing risk substantially.

Initiate Final Approval Without Delay

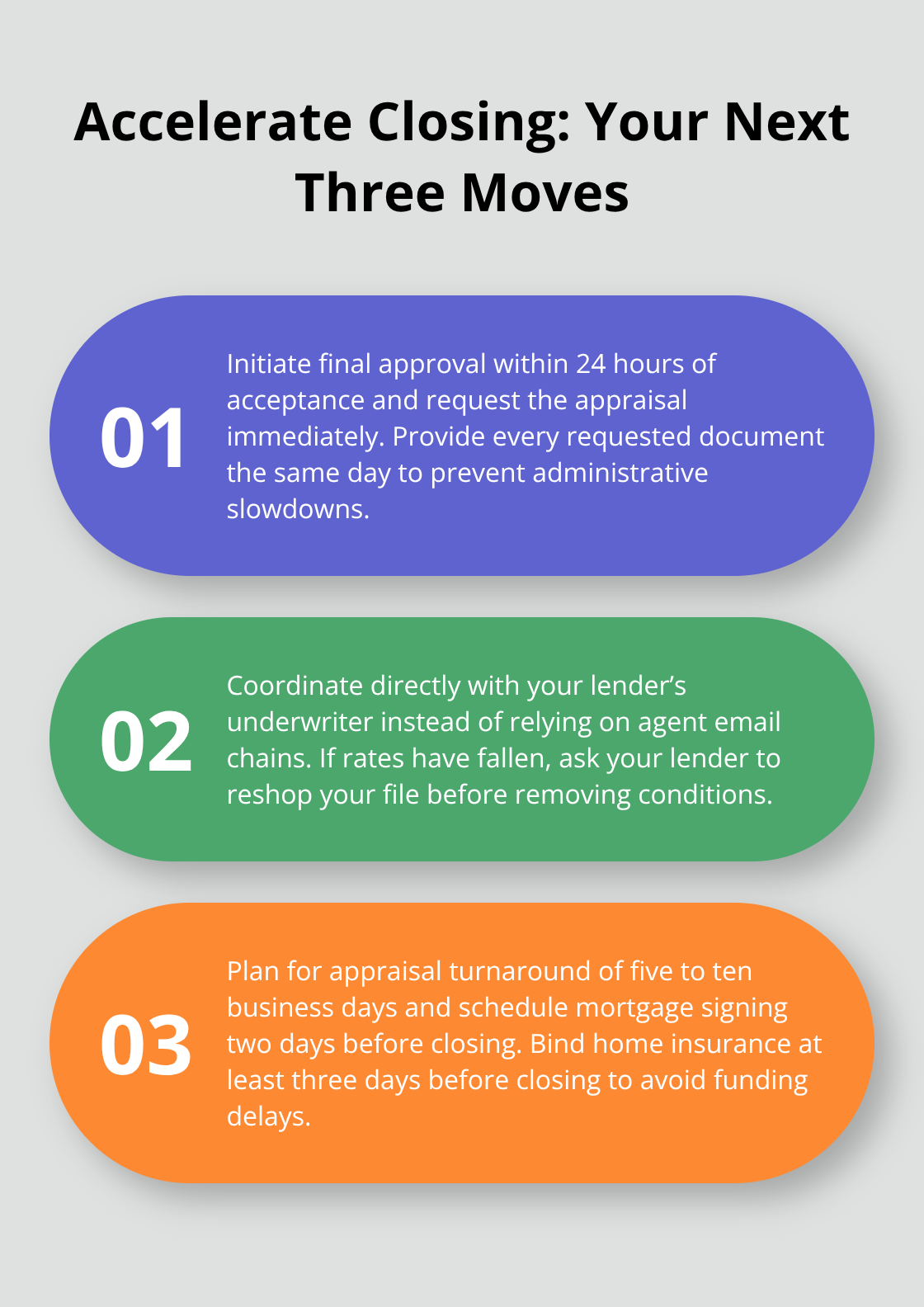

Once your offer is accepted, contact your lender within 24 hours to initiate final approval. Do not wait for the seller’s lawyer to contact you first. Request an appraisal order immediately and provide all requested documentation the same day you receive it to avoid administrative delays.

Final approval typically takes one to two weeks after submission, but only if you respond to lender requests within one business day.

Coordinate directly with your lender’s underwriter rather than relying on email chains with your real estate agent, as brokers often introduce communication lag. If rates have fallen since your preapproval, ask your lender to reshop your file across their lender network before you remove conditions on your offer. Most lenders can capture lower rates within 48 hours if you request it promptly.

Manage Your Appraisal and Insurance Timeline

Hire a lawyer experienced in residential closings immediately after your offer is accepted and ensure your lawyer and lender communicate directly about document timelines. The appraisal typically takes five to ten business days depending on location and appraiser availability, so request it the moment final approval begins. Schedule your mortgage document signing for two days before closing rather than one day before, which gives you a buffer if last-minute issues arise.

Active home insurance is required before mortgage funds release, so obtain quotes from three providers and bind coverage at least three days before closing (this timeline eliminates the common scenario where buyers delay insurance shopping and face funding delays on closing day). Your lender will specify which insurance requirements apply to your specific mortgage product, so confirm those details during your final approval conversation.

Final Thoughts

The most common mistake buyers make is waiting too long to apply for preapproval. Many start house hunting first, then apply, which wastes precious time in competitive markets where properties sell within days. Apply before you view homes so you can move fast when the right property appears. Another frequent error is ignoring your rate lock expiration date and losing rate protection because you failed to reshop your file when rates fell-check that date weekly and contact your lender the moment rates drop.

Buyers also delay final approval by responding slowly to lender requests. When your offer is accepted, treat lender documentation as urgent and respond within one business day, not one week. Coordinate directly with your lender’s underwriter rather than relying on your real estate agent to relay messages, as this eliminates communication delays that push closing dates backward. Following the Canada mortgage preapproval steps we’ve outlined compresses what typically takes months into weeks, giving you genuine speed at closing.

After you receive your preapproval letter, view properties and submit an offer within two weeks. Include your preapproval letter with every offer and state a 30-day closing timeline to signal low risk to sellers. Once your offer is accepted, initiate final approval immediately, order your appraisal the same day, hire a lawyer experienced in residential closings, and bind your home insurance at least three days before closing. We at Financial Canadian help businesses communicate clearly with customers during important transactions, offering responsive designs and SEO best practices to build trust and visibility-whether you’re navigating the mortgage process or running a business, having the right tools accelerates success.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment