Finding the best personal loans in Canada means comparing more than just interest rates. You need to weigh repayment flexibility, fees, and lender reliability against your financial situation.

At Financial Canadian, we’ve built this comparison guide to help you cut through the noise. We’ll walk you through the loan types available, the factors that matter most, and the providers worth considering.

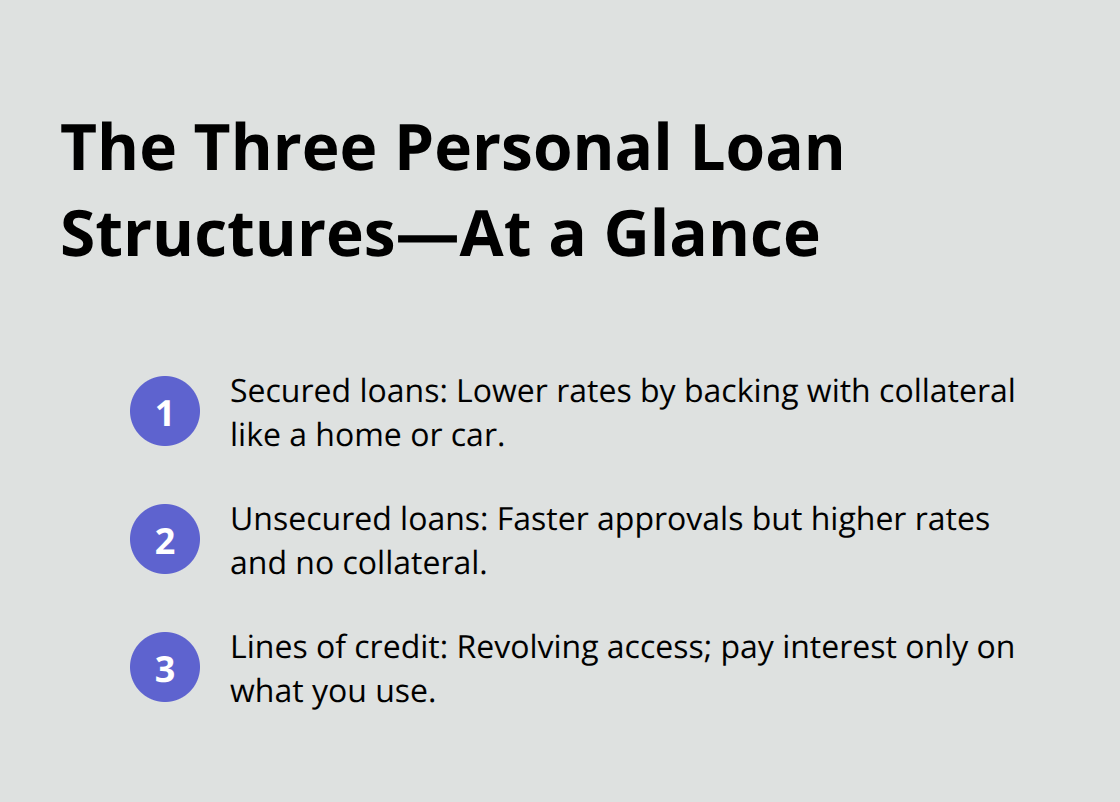

Types of Personal Loans Available in Canada

Canada’s personal loan market offers three main structures, each with different costs and flexibility. Secured loans use collateral like your home or car to back the debt, which lowers the lender’s risk and cuts your interest rate significantly. According to Ratehub data, secured loans for borrowers with poor credit can reach rates around 13%, compared to unsecured options that often exceed 20% for the same credit profile. The tradeoff is real: if you default, the lender can seize your collateral. Unsecured personal loans don’t require collateral, which means higher interest rates but also lower stakes if you hit financial trouble. Traditional banks typically advertise unsecured rates starting around 6% to 10% for well-qualified borrowers, while online lenders and fintech companies charge wider ranges, from 9.90% up to 46.96% depending on credit history and income. Lines of credit work differently-they’re revolving accounts where you draw only what you need and pay interest only on the amount used, not the full credit limit.

Secured Loans Make Sense When You Own Assets

If you own a home with equity, a secured loan becomes your cheapest option. CIBC’s Home Power Plan, for example, uses home equity to secure a lower rate structured as an open line of credit with a promotional rate running until December 6, 2027. The minimum borrowing is $10,000 and requires minimum home equity; you’ll also pay a $300 property valuation fee. The advantage is clear: you access funds flexibly while paying less interest than unsecured alternatives. The risk, however, demands respect-your home serves as collateral, and the lender can force a sale if you default. Origination fees on secured loans typically range from 0.5% to 8% of the loan amount according to Ratehub, so factor these into your total cost before committing.

Unsecured Loans Offer Speed and Simplicity

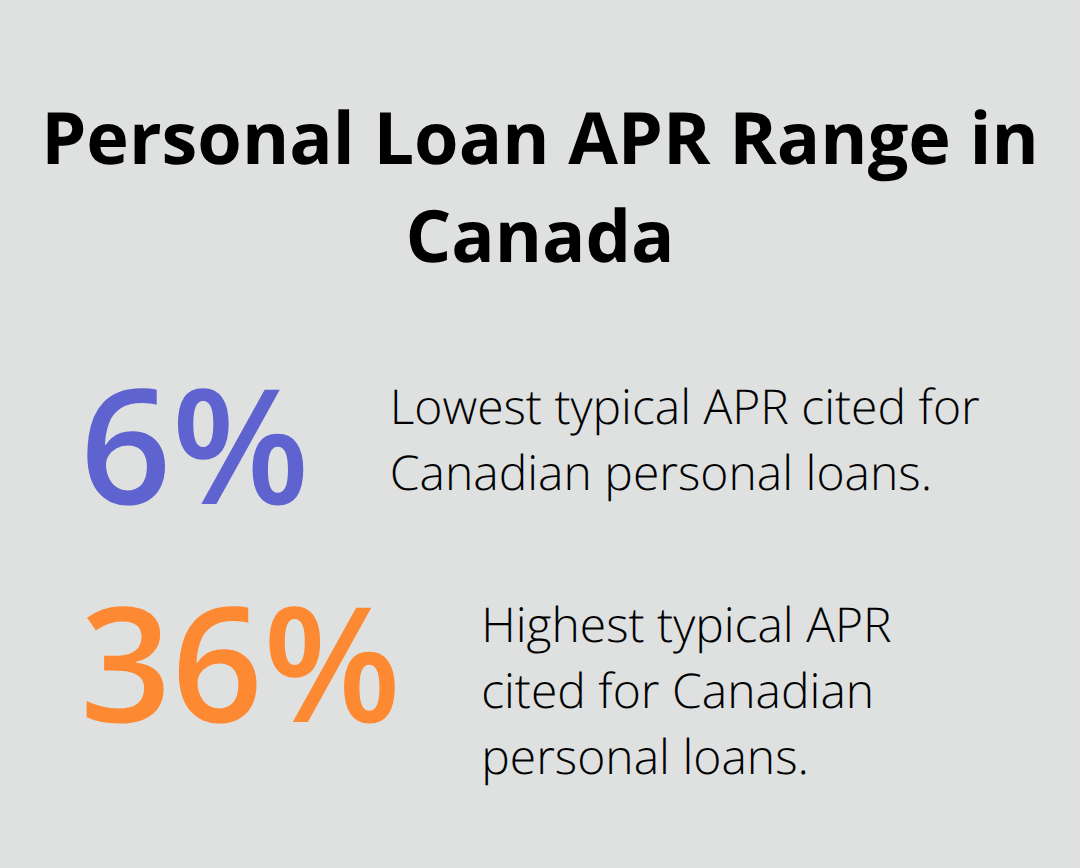

Unsecured personal loans dominate Canada’s market because most borrowers lack significant collateral or prefer not to risk their assets. Banks like Scotiabank, RBC, BMO, TD, and CIBC offer unsecured products with terms from 1 to 5 years, both fixed and variable. Online lenders can approve and fund applications in minutes, making them attractive for emergencies, though their rates reflect higher risk. APRs in Canada range from about 6% to 35% depending on credit history, income, and lender, with the criminal rate of interest capped at 35% APR as of January 1, 2025. When comparing unsecured offers, focus on APR rather than advertised rates-APR includes interest plus fees and shows your true cost. Loan amounts typically range from $100 to $200,000, with terms spanning 6 months to 5 years.

Lines of Credit Give You Flexibility

A line of credit functions as revolving borrowing-you access funds as needed, repay what you borrow, and can draw again. CIBC’s Personal Line of Credit carries interest rates generally lower than many credit cards, and the Home Power Plan offers open-ended terms with flexible access.

Lines work best for ongoing expenses or uncertain cash needs because you avoid the fixed repayment schedule that locks in a personal loan. The downside is that variable-rate lines move with the Bank of Canada target rate; when rates rise, your costs increase. Fixed-rate personal loans, by contrast, keep payments stable regardless of rate changes, making budgeting predictable but potentially more expensive upfront if rates are expected to fall.

Now that you understand the three loan structures available, the next step is identifying which factors matter most when you compare offers from different lenders.

What to Actually Compare When Shopping for a Personal Loan

APR Reveals Your True Borrowing Cost

APR reveals your true borrowing cost; it’s your starting point, but it’s only half the battle. Personal loan APRs range from about 6% to 36%, with rates varying dramatically by credit score tier: borrowers with scores above 800 average around 15.75%, while those below 580 face rates near 30.25%. The gap matters because a 1% difference on a $15,000 loan over five years adds roughly $780 to your total cost. When comparing offers, always request the full APR breakdown, not just the advertised interest rate-this tells you what you’re actually paying after fees are included.

LendingTree users who shop around receive an average of 11 personal loan offers, and choosing the lowest rate saves about $1,659 on average, with potential savings exceeding $3,138 when six or more offers land in your inbox. That’s real money, and it comes from spending 30 minutes comparing lenders instead of accepting the first approval. Origination fees deserve specific attention because they’re often buried in fine print. These fees typically range from 1% to 10% of your loan amount, though some lenders charge higher fees. A $20,000 loan with an 8% origination fee costs you $1,600 before you’ve made a single payment, either reducing the cash you receive or getting added to your balance.

Repayment Terms Shape Your Budget and Total Interest

Shorter loan terms mean higher monthly payments but dramatically lower total interest; a $15,000 loan at 12% costs roughly $1,900 in interest over three years but $4,050 over seven years. LendingTree data shows that borrowers who choose shorter feasible terms pay considerably less overall, yet many default to longer terms simply because the monthly payment feels manageable. Fixed-rate loans lock your payment regardless of what the Bank of Canada does with interest rates, which matters now because the overnight rate sits at 2.25% and could move either direction. Variable-rate loans move with the prime rate, meaning your payment can increase if rates rise, creating budgeting uncertainty.

Lines of credit offer different flexibility entirely: you draw only what you need and pay interest solely on the amount borrowed, not your full credit limit. This works better for ongoing or irregular expenses, but variable-rate lines expose you to rising costs when the Bank of Canada raises rates.

Lender Reputation and Service Quality Matter

Customer service and lender reputation reveal themselves through specific metrics. Check whether a lender offers same-day funding, which several Canadian options including some online lenders now deliver. Verify that a lender accepts co-borrowers or co-signers, because LendingTree data shows this option significantly improves approval odds and can lower your rate. Test the lender’s website tools: a loan calculator lets you estimate real payments before applying, and prequalification features show you personalized offers without affecting your credit score.

Read recent customer reviews on independent sites, but focus on patterns rather than single complaints. Traditional banks like Scotiabank, RBC, BMO, TD, and CIBC offer the lowest starting rates for well-qualified borrowers and provide branch support if you need face-to-face help, while online lenders prioritize speed and approval odds for fair-credit borrowers but typically charge higher rates to offset risk. Your choice between these lender types depends on whether you value the lowest possible rate or the fastest approval process.

Where to Actually Borrow

Banks Offer the Lowest Rates for Strong Credit

Banks dominate Canada’s personal loan market because they offer the lowest starting rates for borrowers with solid credit. Scotiabank advertises rates starting at 6%, RBC from 9%, and BMO from 8.99%, according to Ratehub data. These rates apply only to well-qualified applicants with excellent credit scores and stable income, so don’t assume you’ll land the advertised floor. Your existing bank can approve and fund your application within days, plus you can negotiate terms if you maintain a strong relationship. CIBC offers personal loans with terms from 1 to 5 years, both fixed and variable, and their RRSP Loan lets you borrow up to $75,000 with terms extending to 10 years if you’re using unused contribution room. Traditional banks also provide the widest loan amounts, up to $200,000 in many cases, which matters if you’re consolidating significant debt or funding major expenses. The tradeoff is clear: banks typically require a minimum credit score around 600 and proof of stable income; they won’t approve applicants with recent defaults or collections. If you fall into the fair-credit category, bank approval odds drop sharply, and online lenders become more realistic.

Credit Unions Eliminate Origination Fees

Credit unions fill a specific gap in Canada’s lending landscape. Credit unions like PenFed offer personal loans with no origination fees, which immediately saves you 1% to 8% compared to bank products. This fee elimination matters on a $20,000 loan-you avoid paying $1,600 to $1,600 upfront, either reducing the cash you receive or getting added to your balance. Credit unions typically serve members with fair to good credit and provide competitive rates without the bureaucratic delays that traditional banks impose. Your approval odds improve at credit unions compared to major banks, especially if you maintain an account with them. The downside is that credit unions often cap loan amounts lower than banks do, so they work better for smaller to mid-sized borrowing needs rather than major debt consolidation.

Online Lenders Prioritize Speed Over Rate

Online lenders approve applications in minutes and fund same-day, which beats any traditional institution when you face genuine emergencies. Mogo and Easyfinancial accept borrowers with credit scores as low as 560, though their APRs range from 9.90% to 46.96%, reflecting the risk they absorb. The critical insight: approval speed and willingness to lend to fair-credit borrowers comes at a steep price. A $5,000 loan at 30% costs you $1,600 in interest over three years, compared to $800 at 15% from a bank. Online lenders make sense only when you’ve exhausted traditional options or when the emergency justifies the higher cost. Many online platforms now offer co-borrower options, which LendingTree data shows significantly improves approval odds and can lower your rate if your co-borrower has stronger credit.

Compare Across Lender Types to Quantify Savings

LendingTree users save an average of $1,659 by comparing personal loan offers and choosing the best one. The practical strategy is to apply with your bank first if your credit score exceeds 650, then move to online options only if rejected. Never accept the first approval you receive; compare at least three offers across different lender types to quantify your savings. This comparison takes roughly 30 minutes and can save you thousands over the loan term. Some lenders publish minimum income requirements (CIBC cites about $17,000 gross annual income as a threshold), so verify eligibility before applying. Test each lender’s prequalification tool to see personalized offers without affecting your credit score, which lets you compare real numbers before committing to a formal application.

Final Thoughts

Choosing the best personal loans in Canada requires you to match your financial situation with the right lender and loan structure. Start by pulling your credit report through Equifax Canada or TransUnion Canada, then calculate your debt-to-income ratio to understand how much monthly payment you can realistically afford. This groundwork takes an hour but prevents you from applying to lenders who won’t approve you or accepting terms that strain your budget.

Apply with your bank first if your credit score exceeds 650, since traditional banks offer the lowest rates for strong applicants. If rejected or if your score falls below 650, move to credit unions for competitive rates without origination fees, then online lenders only if you need same-day funding or have fair credit. LendingTree data shows that borrowers who compare just three offers save an average of $1,659, so spending 30 minutes comparing APRs, fees, and terms across lenders directly reduces your borrowing cost.

Calculate your total cost, not just your monthly payment, because a $15,000 loan at 12% costs roughly $1,900 in interest over three years but $4,050 over seven years. Factor in origination fees (which typically range from 1% to 8%) and verify whether your loan allows prepayment without penalty so you can pay it off early if your financial situation improves. At Financial Canadian, we help you compare personal loan options to find the right fit for your situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment