Debt can feel overwhelming, but you’re not alone. Millions of Canadians face this challenge every year, and we at Financial Canadian know that debt relief Canada options exist for nearly every situation.

The path forward depends on your specific circumstances. Whether you’re considering consolidation, a consumer proposal, or bankruptcy, understanding each option helps you make the right choice for your financial recovery.

Consolidating Multiple Debts Into One Payment

Debt consolidation combines multiple debts into a single loan, typically at a lower interest rate than what you currently pay across credit cards and personal loans. In Canada, you can consolidate through banks, credit unions, or alternative lenders, though you should avoid non-bank lenders that charge rates above 10 percent. The math is straightforward: if you carry $15,000 across three credit cards at an average rate of 19.99 percent, consolidating into a single loan at 8 percent saves you roughly $1,800 annually in interest alone.

The Trade-Off: Lower Payments vs. Longer Terms

Consolidation extends your repayment timeline, so while your monthly payment drops, you may pay more interest overall if you stretch payments beyond five years. Balance transfer cards offer another approach-you move high-interest balances to a card offering 0 percent interest for 6 to 21 months, depending on the issuer. This works best if you pay down the balance aggressively during the promotional period; once it expires, rates jump to 19 percent or higher.

The Reaccumulation Trap

One critical mistake people make is accumulating new debt after consolidating, which defeats the entire purpose. You need a strict budget and commitment to stop using credit while you pay down the consolidated loan.

Without this discipline, consolidation merely masks the underlying spending problem.

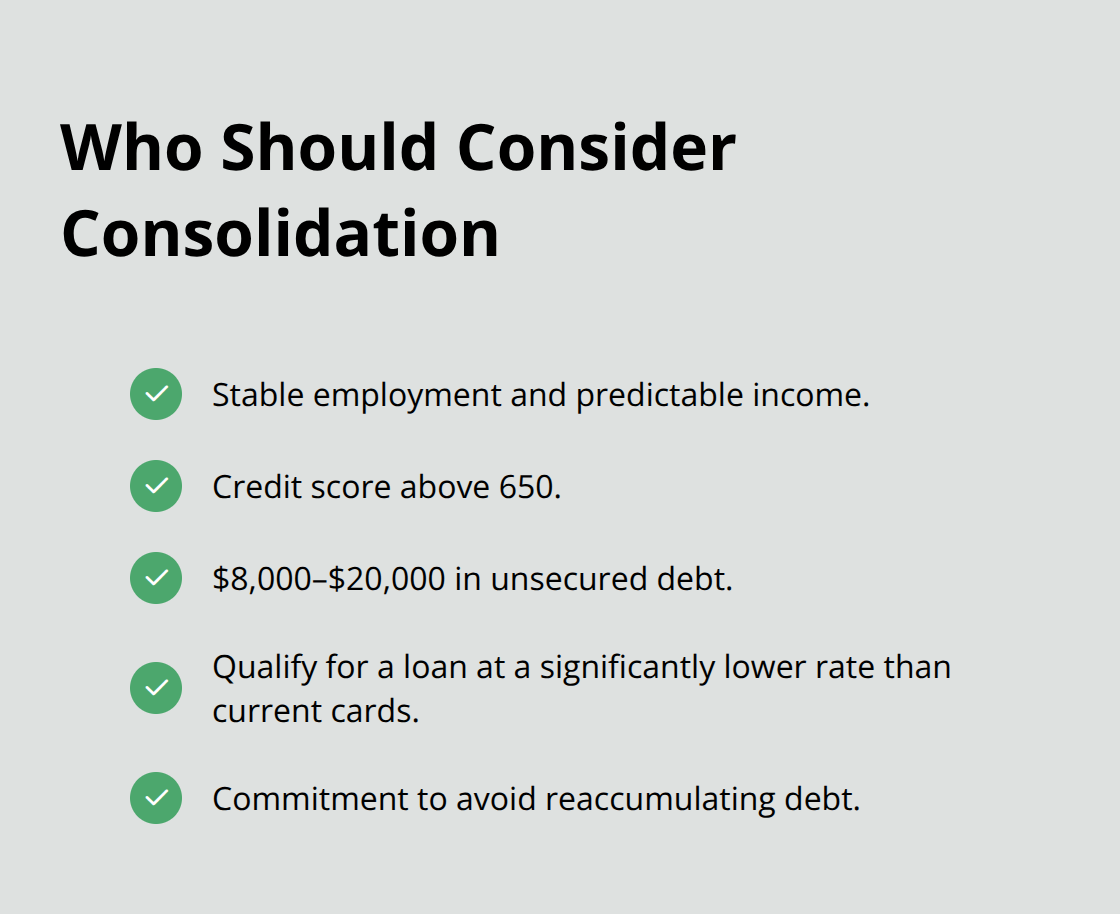

Who Should Consider Consolidation

Consolidation suits people with stable income, decent credit scores above 650, and the discipline to avoid reaccumulating debt. If you carry $8,000 to $20,000 in unsecured debt and can qualify for a loan at a rate significantly lower than your current cards, consolidation cuts both your monthly payment and total interest paid. However, consolidation does not reduce the amount you owe-it only reorganizes it.

When Consolidation Falls Short

If your debt exceeds $30,000, formal options like consumer proposals or bankruptcy may deliver better outcomes. Consolidation also leaves you unprotected against creditor actions; if you miss payments, wage garnishments and collection calls continue. This is why consolidation works best as a preventative step, not a rescue after financial collapse. When consolidation cannot address your situation, formal debt relief programs offer stronger protections and potentially greater debt reduction.

When Formal Debt Relief Makes Sense

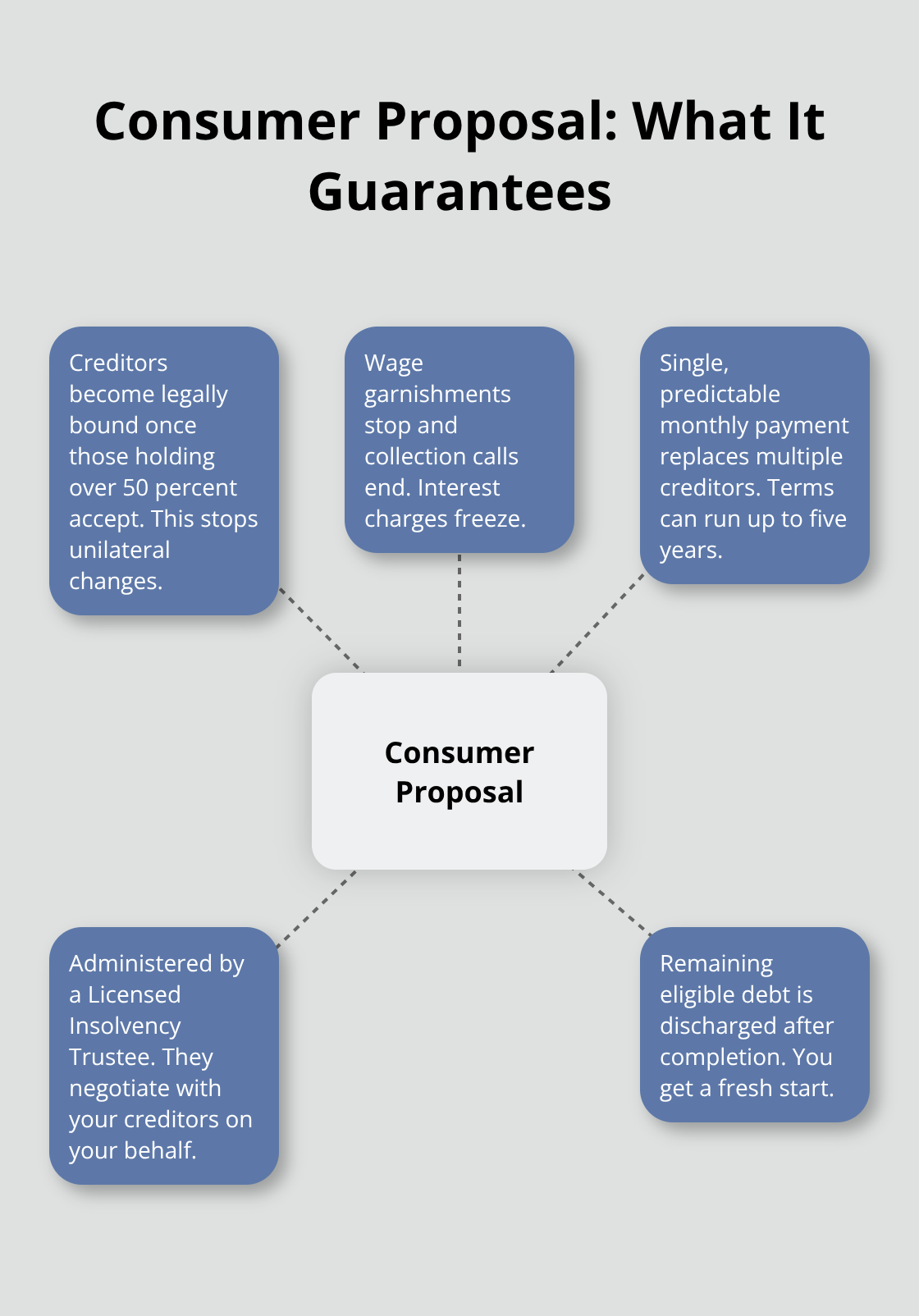

Formal debt relief programs offer legal protection that consolidation cannot match. When your debt exceeds $30,000 or you cannot afford minimum payments, the government-regulated options in Canada are consumer proposals and personal bankruptcy, both administered by Licensed Insolvency Trustees. A consumer proposal lets you settle your debt for a fraction of what you owe-often 20 to 70 percent of your total balance-spread over up to five years. The process is straightforward: a Licensed Insolvency Trustee negotiates with your creditors on your behalf, and once creditors holding over 50 percent of your debt by dollar value accept the proposal, all creditors are legally bound. This means wage garnishments stop, collection calls end, and interest freezes. You make one predictable monthly payment instead of juggling multiple creditors.

Research on Canadian debt relief uptake shows that people with credit card balances around $12,900 and utilization rates near 63 percent are most likely to pursue formal solutions, particularly when monthly obligations become unmanageable.

How Consumer Proposals Work in Practice

Licensed Insolvency Trustees handle the entire negotiation process at no upfront cost to you. They assess your income, assets, and debts, then propose a repayment amount creditors are likely to accept. If creditors reject the proposal, you can modify it or explore bankruptcy instead. The key advantage is that remaining debt gets discharged once you complete the plan, even if you haven’t paid back 100 percent. Your credit score takes a hit initially, but it begins recovering immediately after discharge, and many people rebuild within three to five years. Personal bankruptcy operates similarly but involves surrendering non-exempt assets and typically lasts longer-nine months to two years depending on your income and whether it’s your first bankruptcy. Both options require working with a Licensed Insolvency Trustee; beware of unlicensed debt consultants who charge high fees to do what an LIT provides for free.

Credit Counselling and Debt Management Plans

Non-profit credit counselling agencies offer debt management plans as an informal alternative. These plans consolidate your debts into one monthly payment, and counsellors often negotiate with creditors to reduce or waive interest and fees. Unlike consumer proposals, debt management plans don’t involve court proceedings and don’t require creditor approval to bind them legally. However, they also lack legal protection-creditors can withdraw from the plan or pursue collection actions if you miss payments. A debt management plan typically runs three to five years and works best if you have a steady income and creditors willing to cooperate. The catch is that government creditors and some banks may not participate in informal arrangements, leaving you exposed to collection efforts on those debts. This is why debt management plans suit people with $8,000 to $15,000 in unsecured debt and stable employment; for larger debts or hostile creditors, a consumer proposal provides stronger legal certainty.

Taking the Next Step

Start with a free consultation from a Licensed Insolvency Trustee in your province to compare these options against your specific situation-no referral needed, and you face no obligation to proceed. The trustee will walk you through which path aligns with your income, assets, and goals. Once you understand how formal debt relief works, the practical question becomes how to evaluate which option truly fits your circumstances.

How to Evaluate Your Debt Relief Options

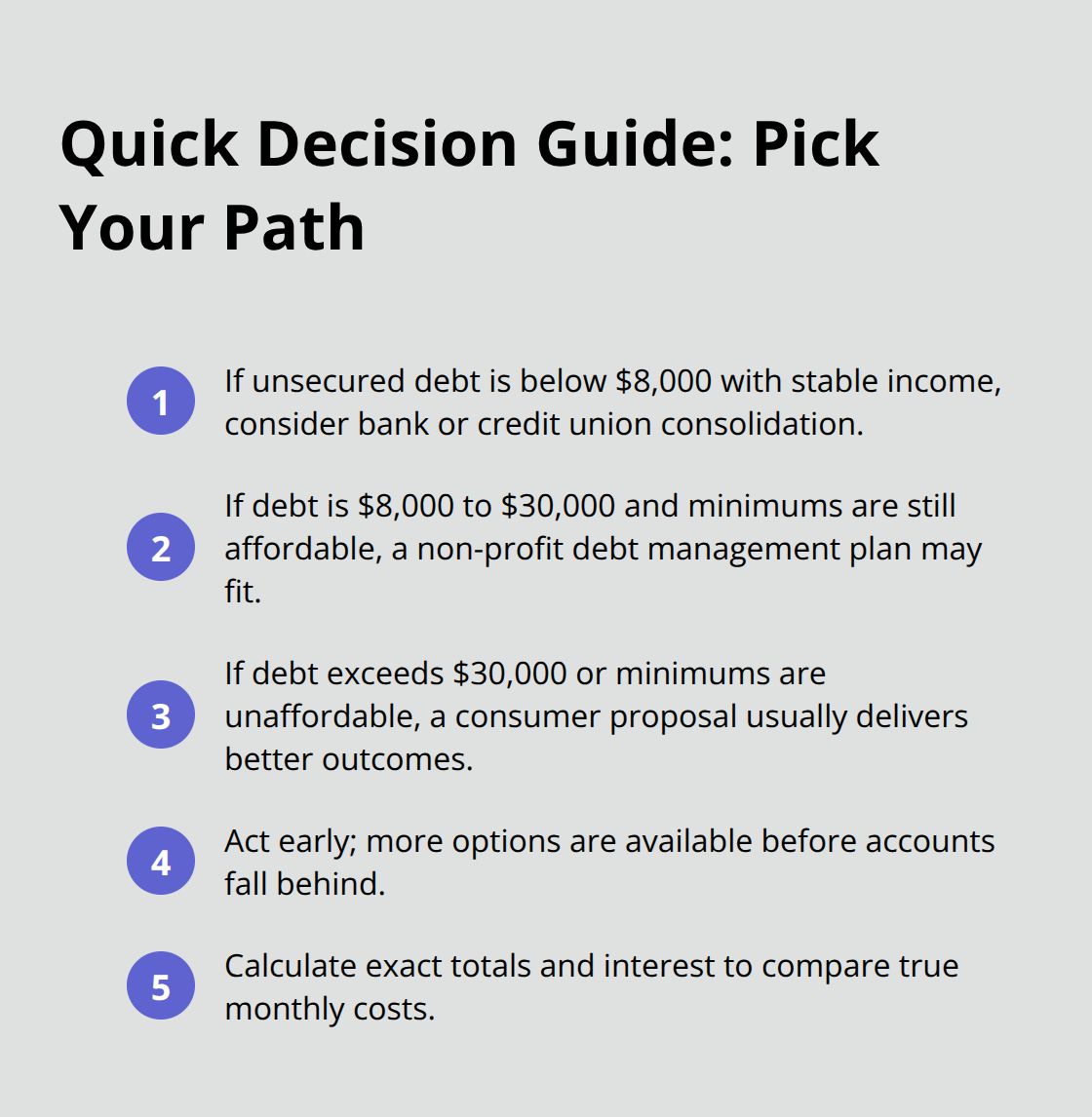

The moment you decide to pursue debt relief, you face a critical decision: which option actually works for your situation? The wrong choice wastes time and money, so this evaluation demands precision, not guesswork. Start by calculating your exact total debt, excluding your mortgage and car loan, then compare it against your monthly household income.

If your total unsecured debt sits below $8,000 and you earn a stable income, consolidation through a bank or credit union often works. If your debt ranges from $8,000 to $30,000 and you can still afford minimum payments with discipline, a debt management plan through a non-profit credit counsellor becomes viable. If your debt exceeds $30,000 or you cannot meet minimum payments, a consumer proposal typically delivers better outcomes than consolidation because it legally reduces what you owe rather than simply reorganizing it.

Research on Canadian debt relief uptake shows that people pursue formal solutions when their situation becomes urgent, but this data masks a critical reality: people often wait too long to act. The sooner you intervene, the more options remain available.

Calculate Your True Monthly Cost

Pull together statements from all your credit cards, personal loans, lines of credit, and any other unsecured debts. Add up the minimum payments across all accounts, then calculate the total interest you pay annually by reviewing each statement’s interest charges for the past year. Most Canadians drastically underestimate this number. If you carry $15,000 across three credit cards at 19.99 percent average interest, you pay roughly $225 monthly in interest alone before touching principal. A consolidation loan at 8 percent cuts that to $100 monthly, freeing $125 for faster payoff.

However, if extending the repayment term from four years to seven years means you pay an extra $3,000 in total interest, consolidation loses its appeal. A Licensed Insolvency Trustee will run these numbers for you during a free consultation and show exactly what each path costs over time. This is not something to estimate yourself; the math must be precise because small differences in rates and terms compound significantly over years.

Compare Timeline and Credit Impact Honestly

Consolidation leaves your credit report intact but doesn’t help your credit score immediately; your score actually drops slightly when you apply for a new loan (due to the hard inquiry and new account). A debt management plan typically runs three to five years, and creditors report it to credit bureaus, which damages your score during the plan but allows recovery once completed. A consumer proposal stays on your credit report for three years after completion, but your score begins improving immediately after discharge because the debt is legally settled.

Personal bankruptcy remains on your report longer and causes more severe damage initially, though recovery is possible within three to five years for many people. The key insight is that formal options often deliver faster credit recovery than consolidation because they provide closure and eliminate the psychological weight of ongoing minimum payments. If you’re choosing between a seven-year consolidation and a five-year consumer proposal, the proposal may actually serve your credit better long-term despite the initial damage. Licensed Insolvency Trustees can project your credit recovery timeline for each option, giving you realistic expectations rather than vague promises.

Talk to a Licensed Insolvency Trustee Now

You’ve read this far, which means you’re serious about change, but reading alone guarantees nothing. Schedule a free consultation with a Licensed Insolvency Trustee in your province immediately. Bring your debt statements, income verification, and list of monthly expenses. The trustee will assess whether you qualify for a consumer proposal, whether bankruptcy makes sense, or whether consolidation remains your best move.

This conversation costs you nothing and obligates you to nothing; the trustee cannot force you into any program. What they will do is eliminate the guesswork that keeps most people paralyzed. They’ll show you the actual monthly payment and timeline for each option, the impact on your credit score, and whether your creditors are likely to accept a proposal (based on your specific financial situation). Many people delay this conversation for months or years, imagining worst-case scenarios that don’t materialize. The reality is almost always less frightening than the anxiety you’re currently experiencing. Licensed Insolvency Trustees handle thousands of cases annually and have seen every financial situation imaginable. Your case is not unique, and your situation is not hopeless.

Final Thoughts

You now understand the full spectrum of debt relief Canada options available to you. Consolidation works when your debt sits below $30,000 and you have stable income and discipline, while debt management plans through non-profit credit counsellors offer a middle ground for debts between $8,000 and $15,000 when creditors cooperate. Consumer proposals deliver legal protection and genuine debt reduction when your situation demands it, and personal bankruptcy remains available as a last resort when other paths won’t work.

The decision between these options hinges on three concrete factors: your total unsecured debt determines which solutions are realistic (consolidation loses appeal above $30,000 because formal options reduce what you actually owe rather than just reorganizing it), your monthly cash flow reveals whether you can sustain any repayment plan, and your timeline matters since a consumer proposal typically beats a five-year consolidation because it provides legal closure and faster credit recovery. What you cannot do is nothing, because every month you delay costs real money in interest and compounds the psychological weight of debt.

Contact a Licensed Insolvency Trustee this week to explore your debt relief options. This conversation is free, confidential, and obligates you to nothing-the trustee will show you exact numbers for your situation, actual monthly payments, real timelines, and honest credit impact projections.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment