When unexpected expenses hit, emergency payday loans in Canada can feel like your only option. But before you apply, you need to understand how they work, what they’ll cost you, and whether they’re actually the right move for your situation.

At Financial Canadian, we’ve put together this guide to help you make an informed decision. We’ll walk you through the application process, show you the real numbers on interest rates, and reveal the alternatives that might save you money.

How Payday Loans Work in Canada

The Application Process and Speed

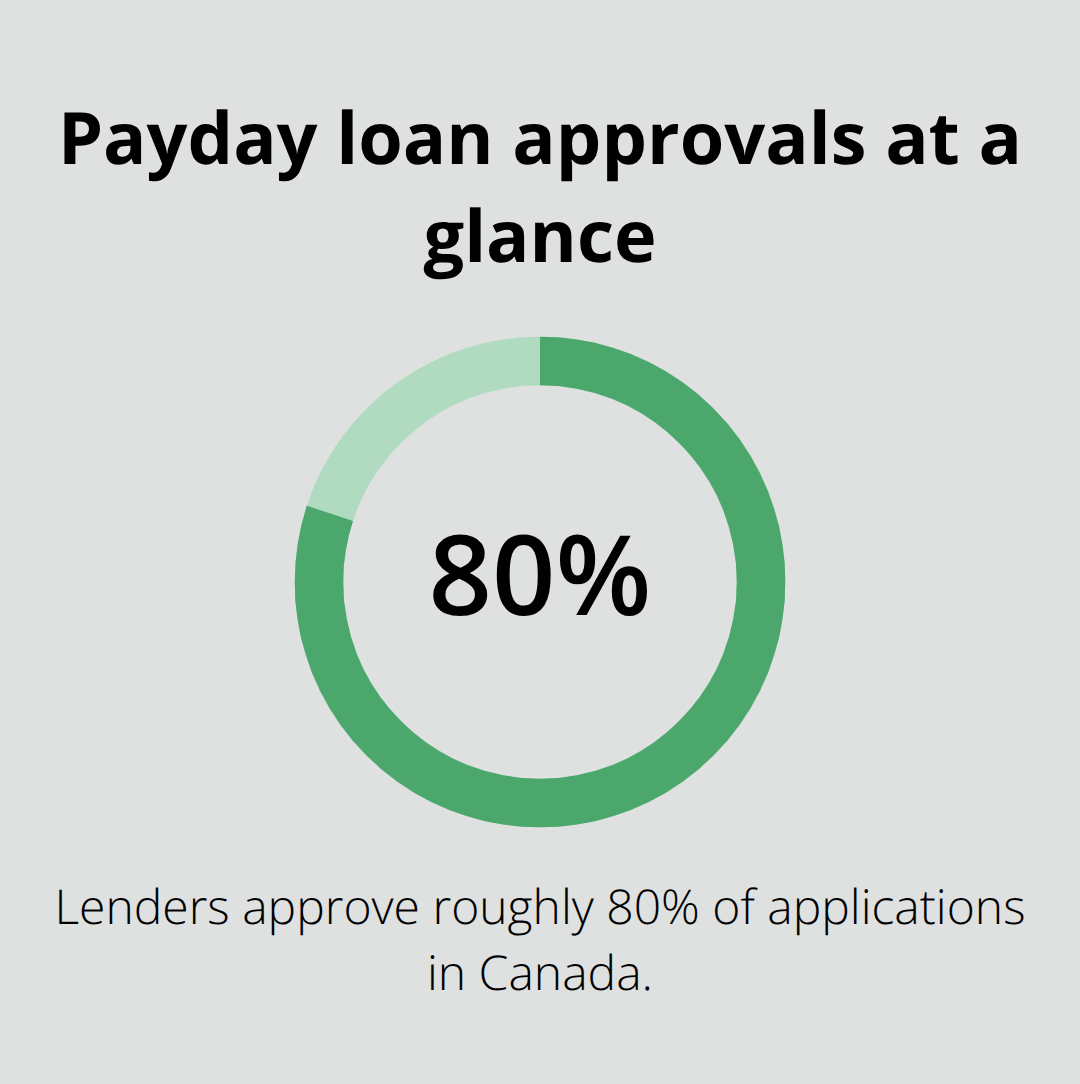

Getting a payday loan in Canada takes anywhere from a few hours to one business day, which is why lenders market them as emergency solutions. You apply online or at a physical location, provide proof of income and a bank account, and if approved, receive cash the same day or within 24 hours. Most lenders require only a government-issued ID, proof of employment, and a recent pay stub showing you earn at least $1,000 monthly. Some lenders skip the credit check entirely, which sounds convenient until you realize they’re betting on extracting fees from borrowers with limited options. The application takes 15 to 30 minutes, and lenders approve roughly 80% of applications, making rejection rare.

The Real Cost of Borrowing

The fees are where payday lenders make their money, and the numbers are staggering. A federal limit on the cost of borrowing for payday loans is $14 per $100 borrowed in all provinces. These aren’t theoretical numbers. A $500 loan costs you $70 in fees alone over two weeks. If you renew that loan because you can’t repay it in full, you pay another $70. High rates and unclear fee structures can lead to payday loan renewal cycles where borrowers become trapped in chronic debt. Lisa Engelkins paid $1,254 in renewal fees to extend a $300 loan across 17 months and 35 renewals. Pamela Gomez took five $500 loans and paid approximately $10,560 in interest with around $880 monthly in fees just to keep the loans active. Most payday borrowers renew their loans four to eight times annually, transforming a short-term cash solution into a long-term debt trap.

Eligibility and Income Requirements

Lenders set eligibility deliberately low to capture desperate borrowers. You need to be at least 18 years old, have a Canadian bank account, and demonstrate steady income. Some lenders accept employment letters, disability payments, or pension income, not just traditional employment. The catch is the repayment requirement: many provinces limit loan amounts to 50% of your net pay or less, meaning if you earn $2,000 monthly after taxes, you can borrow a maximum of $1,000. New Brunswick is stricter, capping loans at 30% of net pay. Lenders verify income through bank statements or pay stubs, taking roughly five to ten minutes to confirm you can technically repay. However, lenders rarely assess whether you can actually afford to repay and cover living expenses simultaneously. Most borrowers who take payday loans live paycheck to paycheck, and a $500 loan represents money they don’t have. Lenders don’t care about that reality because their profit comes from fees, not successful repayment. A 2018 study from the Global Financial Literacy Excellence Center at George Washington University found that 42% of millennials have used payday loans to cover bills or debt, showing how widespread this desperation is across age groups.

Why Renewal Traps Borrowers

What matters far more than approval speed is understanding what happens after you borrow. Lenders structure loans to encourage renewal rather than full repayment. When you can’t pay the full amount due, lenders allow you to pay only the initial fee to extend the due date, creating a cycle of additional fees. This design isn’t accidental-it’s the business model. Borrowers who intended to repay in two weeks find themselves trapped for months or years, paying hundreds of dollars in fees while the principal barely shrinks. The debt cycle persists because lenders renew or re-balance loans instead of offering real solutions. Some borrowers carry nine or more payday lenders at once, shuttling between lenders to pay fees and avoid default. The cumulative cost of small loans far exceeds the original principal due to repeated fees and renewals. Understanding this trap is essential before you consider applying, because the speed and ease of getting approved masks the financial damage that follows.

The Real Trade-Off Between Speed and Cost

Payday loans offer one genuine advantage: speed. When your car breaks down and you need $800 for repairs to keep your job, a payday lender delivers cash within hours while banks require days and credit card applications take weeks. That speed matters when you’re facing eviction, a utility shutoff, or a medical bill your employer won’t cover. However, speed is the only advantage worth discussing, and it comes with a financial price so steep that most borrowers would be better off exploring alternatives first.

The cost structure of payday loans makes them genuinely dangerous for anyone without a solid plan to repay within two weeks. A $500 loan at the federal maximum of $14 per $100 borrowed costs $70 in fees over 14 days, which equals an effective annual percentage rate of roughly 350%. Credit cards typically charge 15 to 30 percent APR, making them dramatically cheaper even when you carry a balance. Personal loans from banks or credit unions cost even less, usually between 5 and 12 percent APR. The speed advantage disappears entirely if you need to renew the loan because you couldn’t repay it in full. Once you renew, you’ve paid $140 in fees on a $500 principal that hasn’t shrunk. After four renewals, you’ve paid $280 in fees while owing the full $500 principal.

Arthur Jackson started with a $200 payday loan and ended up paying roughly $5,000 in interest due to more than 100 renewals. Speed becomes a trap when the lender’s business model depends on you renewing repeatedly.

How Payday Loans Destroy Your Budget

The real damage happens when you factor payday loans into your actual monthly expenses. If you earn $2,500 monthly after taxes and take a $500 payday loan, you’re now committing $70 every two weeks to that loan fee alone. Over a month, that’s $140 in fees just to keep one loan active. Add rent, utilities, groceries, and transportation, and you’ve already exceeded your income.

Most borrowers who take payday loans report paying fees before essential living costs like rent, utilities, and groceries, creating acute budget pressure that forces them to take additional payday loans. Mary Hamilton reported paying over 40 percent of her monthly income in fees across multiple lenders. The debt cycle persists because once you’ve taken one payday loan, you lack the funds to cover the next emergency without taking another one. Lenders understand this completely and structure their business around it. They don’t profit from borrowers who repay once; they profit from borrowers who renew four to eight times annually.

What Actually Works When You Need Emergency Cash

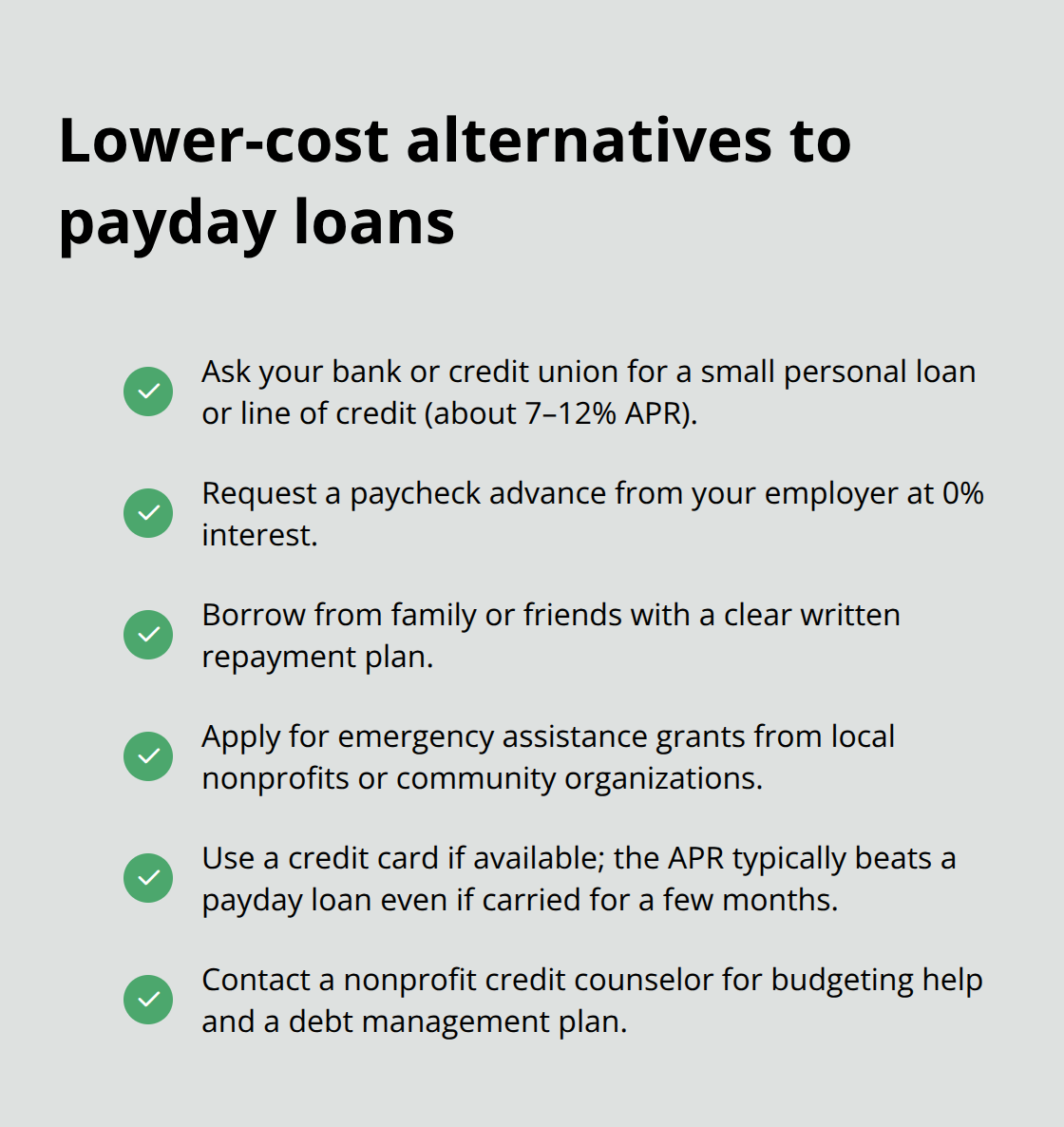

Before applying for a payday loan, contact your bank or credit union about a personal line of credit or small personal loan, which typically charge 7 to 12 percent APR and allow repayment over months rather than weeks. Many employers offer emergency advances against your next paycheck with zero interest; ask your HR department whether this option exists. If you have family or friends who can lend you money, ask them directly and offer to repay on a set schedule.

Contact local nonprofits or community organizations that offer emergency assistance grants for specific situations like utility bills or medical costs; these require no repayment. If you have a credit card, the interest rate almost certainly beats a payday loan, even if you carry the balance for three months. For ongoing financial stress, contact a credit counselor through a nonprofit credit counseling agency, which offers free budgeting help and debt management plans.

These alternatives require more effort than filling out an online payday loan application, but they cost a fraction of what payday lenders charge and won’t trap you in a renewal cycle that lasts months or years. Understanding which option fits your situation determines whether you escape an emergency or create a financial crisis that lasts far longer than the original problem.

How Canadian Payday Loan Regulations Actually Protect You

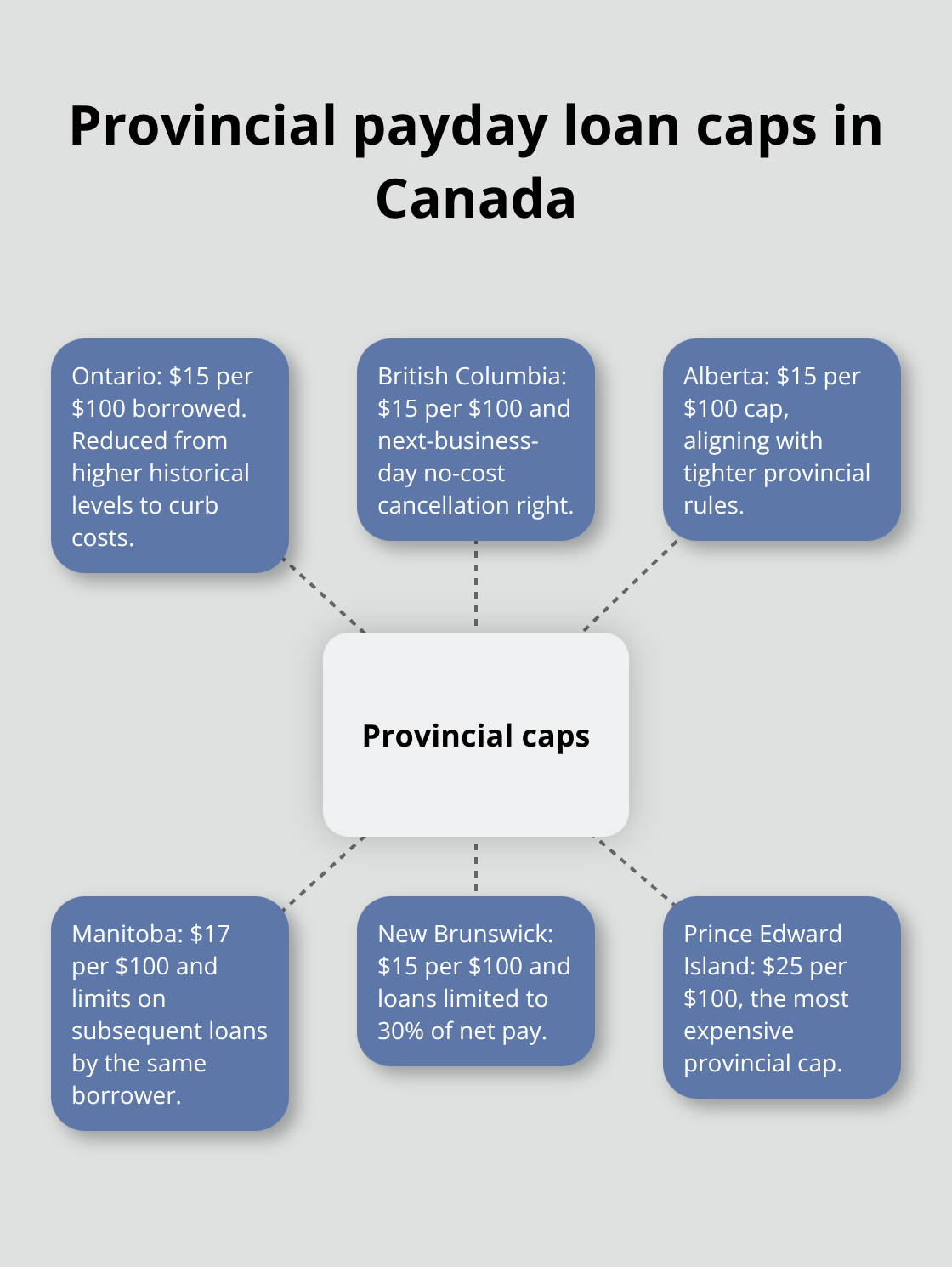

Every province in Canada regulates payday lending differently, and understanding your provincial rules is the difference between knowing your rights and getting trapped by a predatory lender. The federal government set a maximum of $14 per $100 borrowed, but provinces impose stricter caps in most cases.

Ontario reduced its maximum to $15 per $100 in 2018, which equals roughly 3,724% annualized, down from the original $21 per $100 that lenders charged before 2008. British Columbia tightened rules to the same $15 per $100 cap effective January 1, 2017, and added protections that allow borrowers to cancel loans by the end of the following business day at no cost. Alberta matches this $15 per $100 cap, while Manitoba caps payday loans at $17 per $100 every two weeks and limits subsequent loans by the same borrower to 5% within a specified period. New Brunswick requires lenders to be licensed with the Financial and Consumer Services Commission and caps fees at $15 per $100, but also limits loan amounts to just 30% of net pay-the strictest income-based restriction in Canada. Nova Scotia caps loans at $17 per $100 with late charges up to $40, a significant reduction from the $31 per $100 rate that existed before 2018. Prince Edward Island allows $25 per $100 borrowed for two weeks, yielding an extremely high effective APR of roughly 33,519%, making it the most expensive province for payday borrowing. Quebec effectively bans the typical payday-loan model by limiting the effective APR to 35%, forcing lenders to offer installment plans rather than two-week balloon payments. Saskatchewan’s 2010 framework includes a 23% cap on the principal with a 30% cap on defaulted loans. Know your provincial rules before you apply, because they directly determine how much you’ll pay and what protections you receive.

Your Right to Cancel and What Lenders Must Disclose

Most provinces now require payday lenders to register with a provincial regulator and disclose the total cost of borrowing in writing before you sign. British Columbia requires lenders to register with Consumer Protection BC and prohibits issuing more than one loan at a time or requiring repayment exceeding 50% of take-home pay. New Brunswick’s FCNB requires borrowers to cancel within 48 hours at no charge, giving you a cooling-off period to reconsider. Many provinces mandate that lenders disclose the APR, the total fees, and the repayment date in clear language, not buried in fine print. If a lender refuses to provide this information in writing or pressures you to sign without reviewing the disclosure, that’s a red flag that you’re dealing with someone operating outside provincial rules. Contact your provincial consumer protection office immediately if this happens. Some lenders still attempt to access borrowers’ bank accounts for repayment, a tactic that triggers overdraft fees and additional penalties when funds aren’t available. Provincial regulations increasingly restrict this practice, but enforcement varies. Never authorize automatic bank withdrawals unless you’ve verified the exact amount and date in writing.

Identifying Predatory Practices Before You Borrow

Predatory lenders rely on desperation and speed, counting on borrowers to sign without reading the terms. A legitimate lender will provide a written contract at least 24 hours before you must repay, explain the renewal process in detail, and answer questions about what happens if you can’t repay. Lenders who refuse to discuss alternatives, pressure you to borrow more than you requested, or guarantee approval without verifying your income are operating predatory tactics. Some lenders threaten legal action to pressure continued payments, a practice that violates consumer protection laws in most provinces. If a lender threatens legal action, document the threat and report it to your provincial regulator. The Kilroy v. A OK Payday Loans case in British Columbia in 2006 found that certain processing and deferral fees constituted interest, leading to a substantial payout and establishing precedent that lenders cannot hide interest charges as processing fees. Use this case as proof that courts will side with borrowers when lenders misrepresent fees. Contact your provincial consumer protection agency or the Financial Consumer Agency of Canada if you believe a lender has violated regulations or engaged in predatory practices. If you’re struggling with payday debt, debt consolidation and credit score monitoring are alternatives worth exploring to protect your financial health.

Final Thoughts

Payday loans make sense only in narrow circumstances where you need cash within hours and have exhausted every other option. If your car won’t start and you’ll lose your job without transportation, or your landlord threatens eviction in 48 hours, emergency payday loans in Canada might prevent worse financial damage. Contact your bank about a personal line of credit, ask your employer for an advance, or reach out to local nonprofits offering emergency assistance before you apply, because these alternatives cost a fraction of what payday lenders charge.

The reality is that payday loans trap far more borrowers than they help. Lisa Engelkins, Pamela Gomez, and Arthur Jackson took loans for genuine emergencies and got caught in renewal cycles that lenders deliberately engineer (consuming hundreds of dollars monthly in fees while the principal barely shrinks). A credit card charges 15 to 30 percent APR compared to payday loans at roughly 350 percent, and a personal loan from your bank or credit union costs 5 to 12 percent APR with repayment over months instead of weeks.

If you’re already trapped in payday debt, contact a nonprofit credit counselor immediately for free budgeting help and debt management plans. We at Financial Canadian recommend exploring debt consolidation options to protect your financial stability. Take time to understand your provincial protections and alternatives before applying, because the cost of payday borrowing extends far beyond the fees you’ll pay.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment