Getting approved for a payday loan in Canada requires meeting specific lender expectations. At Financial Canadian, we’ve found that most borrowers don’t realize how straightforward these payday loan requirements Canada actually are.

The good news is that lenders focus on practical factors like income and employment status rather than perfect credit scores. This guide walks you through exactly what lenders look for and how to strengthen your application.

Income and Employment Verification

Payday lenders focus on one thing: can you repay the loan on your next payday? This means they care far less about your credit score and far more about proof that money regularly hits your bank account. Most lenders require proof that you have a regular income, though specific minimum amounts vary by lender. The fastest way to prove this is through recent pay stubs, typically from the last 30 days, showing your employer name, pay frequency, and net income. Direct deposit records work equally well-lenders can see your transaction history and confirm that payday deposits arrive consistently. Lenders run income verification as one of their five core checks before approval, and mismatches between what you claim and what your documentation shows cause quick rejections.

What Pay Stubs Reveal

Your pay stub matters more than your job title. Lenders examine net income, not gross salary, because that’s what you actually have available to repay. The name on your pay stub must match your ID exactly-even small typos trigger rejections. If you’ve recently changed jobs, bring pay stubs from both employers to show continuity of income. Lenders also look at pay frequency: weekly, biweekly, or monthly payments all work, but they’ll schedule your repayment around your typical payday. Bank statements covering the last 30 to 60 days work as backup proof, allowing lenders to see your deposit history directly. Some lenders contact your employer briefly to confirm employment status and income level, so keep your employer contact information on your application current and accurate.

Self-Employment Documentation

Self-employed borrowers face stricter scrutiny and typically must provide recent tax returns, invoicing records, or both to demonstrate steady cash flow. Lenders want to see that your income is predictable and arrives on a regular schedule. Without traditional pay stubs, you’ll need additional paperwork compared to salaried workers. Recent business bank deposits serve as proof of income when direct deposit isn’t available through an employer. The key is showing consistent earnings over time-sporadic or declining income raises red flags during the approval process.

Direct Deposit Strengthens Your Application

Lenders heavily prefer applicants with active direct deposit because it proves stable income and provides a clear repayment timeline. When you receive funds via direct deposit, lenders schedule your loan repayment to align with your payday, reducing default risk significantly. This is why most payday lenders require you to have a Canadian bank account in your own name that accepts direct deposits and maintains enough funds to cover repayment. If you don’t have direct deposit set up, contact your employer’s payroll department and request it-this single step strengthens any loan application. Self-employed individuals without traditional direct deposit can use recent business bank deposits as proof instead (though this requires additional documentation compared to salaried workers). Once you’ve confirmed your income meets lender requirements, the next step involves understanding how lenders assess your financial history and credit situation.

Credit Score and Financial History

Payday lenders operate on a fundamentally different principle than traditional banks: they assess your next paycheck, not your past financial mistakes. This distinction changes everything about approval odds. While a low credit score might trigger rejection at a bank, payday lenders often approve applicants with poor credit, previous defaults, or even active collections accounts. The reason is straightforward-they lend against your income, not your creditworthiness. Lenders run alternative risk assessments that focus on employment stability and banking patterns rather than credit bureau reports. Your credit score matters far less than whether you can show consistent income deposits into a Canadian bank account. That said, bad credit doesn’t guarantee approval at the lowest rates. Applicants with damaged credit histories typically qualify for smaller loan amounts, face higher interest rates within the lender’s approved range, or encounter stricter income verification requirements.

What Bad Credit Actually Means for Your Application

Some lenders request additional documentation from bad-credit applicants-extra pay stubs, longer bank statements, or proof of steady employment beyond standard requirements. A few specialized lenders require a guarantor or co-signer when approving poor-credit borrowers, though this remains uncommon in the Canadian payday market. The key insight: bad credit shifts the approval process, not the outcome. You face rejection only if you cannot prove stable income; your credit history alone won’t disqualify you.

Recent Banking Activity Predicts Repayment Better Than Credit History

Recent banking activity predicts repayment behavior rather than reviewing your full credit history. When you submit bank statements covering the last 30 to 60 days, lenders look for consistent income deposits and available account balances-not your credit score. If your statements show regular paycheck deposits and sufficient funds to cover the loan repayment, approval becomes likely even with past defaults or missed payments on credit cards. This is why lenders request proof of a stable income stream; they bet on your next paycheck, not your past behavior. Late payments on previous payday loans carry more weight than old credit card debt because they signal difficulty repaying similar short-term obligations.

How Responsible Repayment Rebuilds Your Credit

Some lenders report payment history to Equifax Canada, which means responsible repayment of a payday loan can actually help rebuild your credit score over time. This creates an opportunity: if you carry bad credit, a payday loan managed responsibly-borrowed only for genuine emergencies and repaid on schedule-demonstrates creditworthiness to future lenders. Conversely, defaulting on a payday loan compounds credit damage and makes future borrowing significantly harder.

Existing Debt Reduces Loan Size But Doesn’t Block Approval

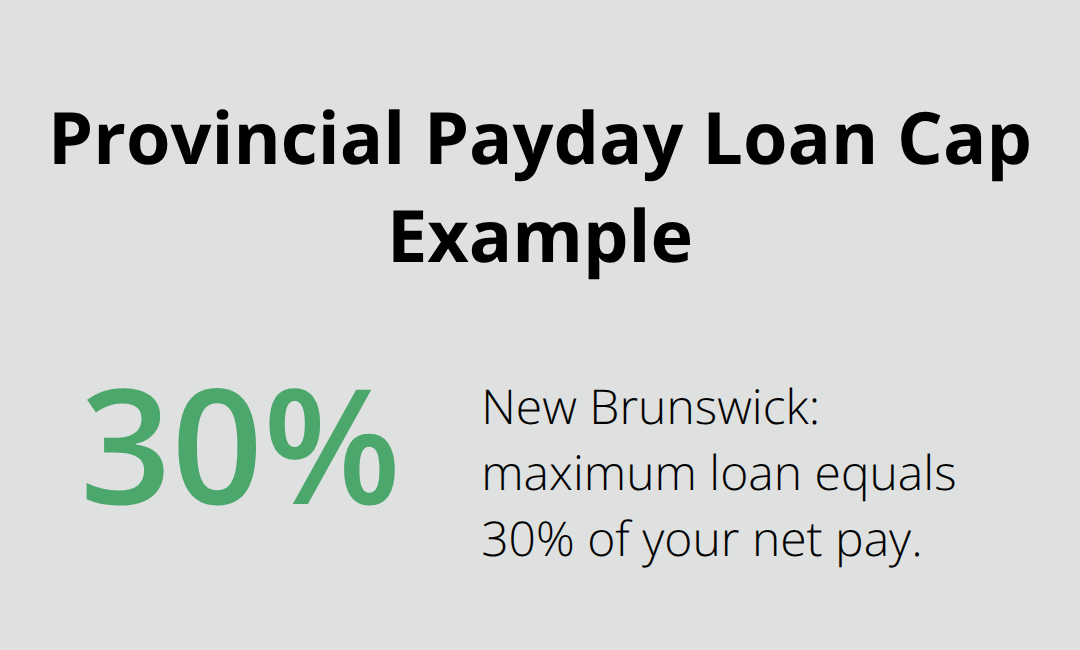

Payday lenders don’t reject applicants simply because they carry existing debt-mortgages, car loans, credit card balances, or past-due accounts. What matters is whether your next paycheck covers the payday loan repayment without leaving you unable to pay rent or essential bills. Lenders assess your net income against the proposed repayment amount, not your total debt load. If you earn $2,000 biweekly and request a $500 payday loan, the lender calculates whether $500 can be repaid from that $2,000 without creating hardship. Provincial regulations reinforce this approach. New Brunswick caps payday loans at 30 percent of your net pay.

These caps exist precisely because lenders recognize that existing obligations already consume much of your income. Higher existing debt doesn’t automatically disqualify you, but it does reduce the maximum loan amount you can access. If you carry significant existing debt and need a larger loan, expect approval for a smaller amount than you requested. Being honest about your financial obligations during the application process matters-lenders verify income and banking patterns anyway, and misrepresenting your situation only leads to rejection or approval for amounts too small to solve your actual problem. Understanding how lenders assess your financial situation sets the stage for the next critical requirement: proving your identity and establishing the legal foundation for your loan.

Personal Identification and Bank Account Requirements

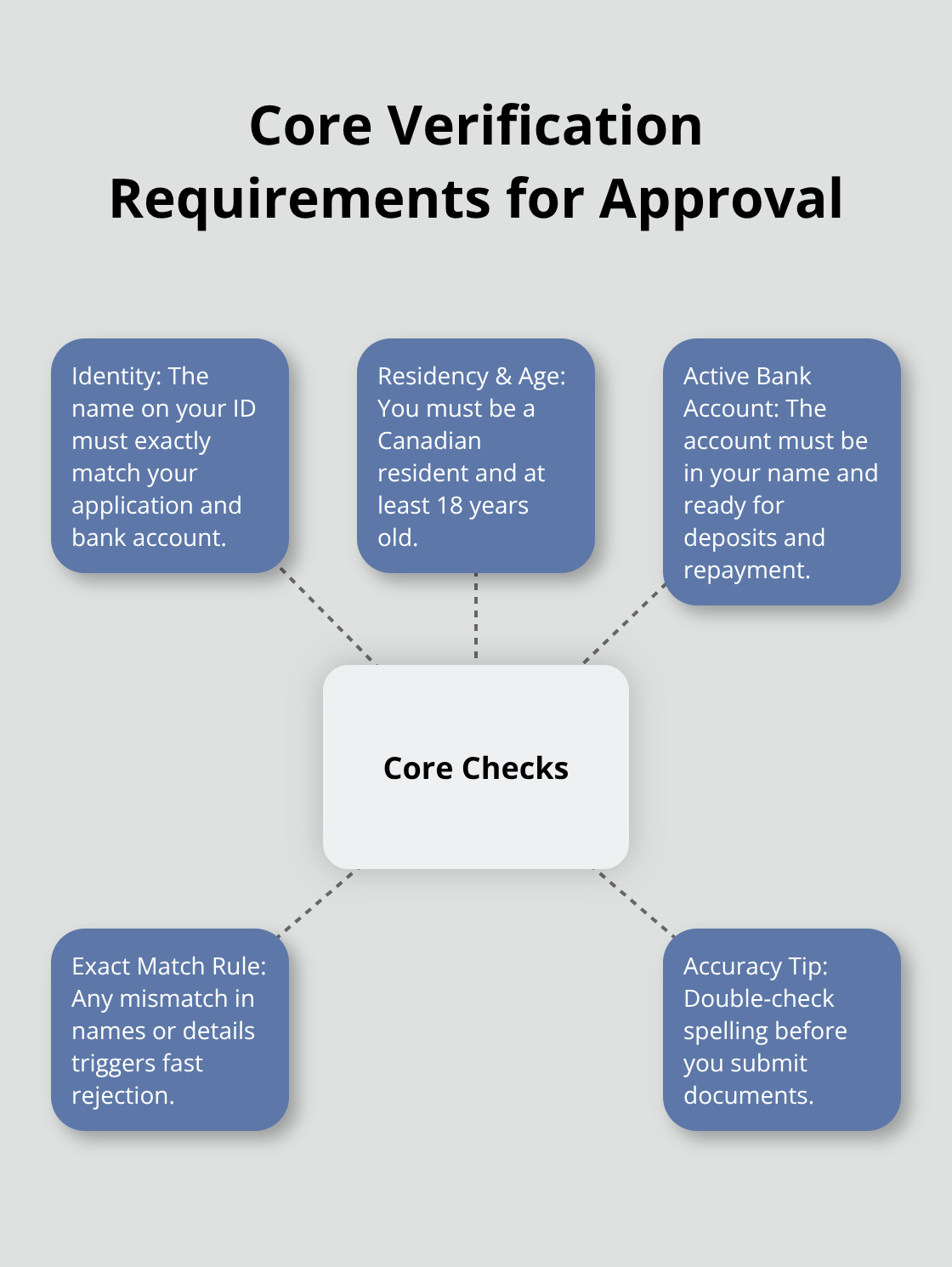

Payday lenders verify three critical elements before approving your application: your identity, your Canadian residency and age, and your active bank account for repayment. Government-issued photo identification is non-negotiable. Your driver’s license, passport, or provincial ID card must match the name on your bank account and pay stubs exactly. Mismatches between your ID and application details trigger automatic rejections, so verify spelling before submitting anything.

Government-Issued ID and Residency Proof

Lenders confirm your residency by matching your address to your ID, and some request a utility bill or lease agreement as secondary proof. You must be 18 or older to qualify, and you must be a Canadian resident. The Social Insurance Number may be requested during application, but lenders do not use it for credit scoring-they use it purely for identity verification and income confirmation. Having your SIN ready speeds up the process, though some lenders operate without requiring it at all.

Your Canadian Bank Account: The Foundation of Approval

Your Canadian bank account is the final piece of the approval puzzle. The account must be in your name, active, and capable of receiving direct deposits or Interac e-Transfer funds. Lenders examine your account to confirm it has enough balance to cover the repayment amount when your next paycheck arrives. If your account is perpetually overdrawn or has insufficient funds available, lenders see higher default risk and may deny approval or offer smaller amounts.

Set up direct deposit with your employer if you haven’t already-this single step removes friction from the entire approval process and signals financial stability to lenders. Ensure your bank account details on the application match your ID exactly. If you recently changed banks, update your employer’s payroll records and provide your new account information to the lender. Some lenders accept prepaid cards that support direct deposits, though traditional chequing accounts are preferred.

Transfer Limits and Funding Methods

Interac e-Transfer limits cap transfers at $10,000 per transaction (depending on your bank’s processing limits), so if you need funds above that threshold, confirm your lender offers direct deposit as an alternative. Direct deposit removes the transfer-limit constraint entirely and allows lenders to schedule repayment around your payday automatically. Having everything aligned-matching ID, current address, active direct-deposit-enabled bank account, and proof of income-removes barriers to approval and moves you toward funding within 48 hours or faster in some cases.

Final Thoughts

Payday loan requirements Canada boil down to three core factors: proof of regular income, valid identification, and an active Canadian bank account. We at Financial Canadian have observed that most borrowers stress about credit scores when lenders focus primarily on your next paycheck. Meeting these straightforward requirements dramatically improves your approval odds and accelerates funding timelines.

Gather your recent pay stubs or bank statements that show consistent income deposits, verify your government-issued ID matches your application details exactly, and confirm your bank account is active and ready to receive funds. Self-employed applicants should add recent tax returns or invoicing records to strengthen their case, and setting up direct deposit with your employer removes friction from the entire process. Bad credit won’t disqualify you, and existing debt won’t block approval-what matters is demonstrating that you earn money regularly and can repay the loan from your next paycheck.

Once you’ve confirmed you meet these requirements, compare payday lenders in your province to find one that matches your needs. Review interest rates and fees, verify the lender is properly licensed or registered with your provincial authority, and read the full loan agreement before signing. Responsible borrowing-using payday loans only for genuine emergencies and repaying on schedule-can actually help rebuild your credit if the lender reports to Equifax Canada.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment